Payment rails are the infrastructure that enables the transfer of money between banks, financial institutions, and individuals. For businesses, choosing the right payment rail depends on factors like speed, cost, geography, and customer satisfaction.

ACH and Zelle are two common payment rails in the United States. ACH is used for batch processing of transactions, while Zelle offers real-time transfers between participating banks. Lightspark aims to move past these traditional rails by leveraging Bitcoin’s decentralized foundation to create a more efficient global payments network.

The Payment Rail Landscape

Payment rails are crucial for moving money between parties, but current systems can be slow, fragmented, and costly, often leading to inefficiencies and higher expenses for businesses and consumers alike.

Understanding ACH and Zelle

How ACH Works

The Automated Clearing House (ACH) is an electronic funds-transfer system managed by Nacha. It processes large volumes of credit and debit transactions by batching them together and processing at specific intervals. An ACH transaction starts when an originator initiates a direct deposit or payment. The originator's bank (ODFI) collects and batches these requests, sending them to an ACH operator (Federal Reserve or clearinghouse). The operator sorts and distributes the transactions to the recipient's bank (RDFI), which then credits or debits the recipient's account. This system supports both domestic and international transactions, with recent updates allowing for same-day settlements.

Strengths and Limitations of ACH

Strengths

- Makes online transactions quick and easy by batching and processing them at specific intervals.

- Offers cost-effective transfers, often cheaper than wire transfers and suitable for a wide range of transactions.

- Provides a reliable and established method for various types of electronic payments, including payroll deposits and bill payments.

Limitations

- Transactions are not instant and can take one to three business days to settle.

- Some banks may impose limits on the amount of money you can transfer, requiring multiple transactions for larger amounts.

- Fees may apply for ACH transactions, which can accumulate if you perform multiple transactions.

How Zelle Works

Zelle® operates by linking users' eligible checking or savings accounts to their email addresses or U.S. mobile phone numbers. Integrated into the Wells Fargo Mobile® app and Wells Fargo Online®, it allows for quick money transfers between U.S. bank accounts. To use Zelle®, users enroll through their bank's digital platform, add trusted contacts, and select the send or request function. The recipient is notified via email or text. If not enrolled, they receive instructions to do so. Once enrolled, funds are typically available within minutes. Zelle® is designed for transactions with known and trusted individuals or businesses.

Strengths and Limitations of Zelle

Strengths

- Zelle® offers real-time or near-real-time transfers, making it one of the fastest options for sending money between U.S. bank accounts.

- There are no fees for using Zelle® through Wells Fargo, making it a cost-effective choice for personal transactions.

- It is integrated into existing banking apps, providing a seamless and convenient user experience without the need for a separate app.

Limitations

- Zelle® transactions are irreversible, so users must be certain of the recipient's identity before sending money.

- There is no purchase protection, meaning users are not covered if they do not receive the item or service they paid for.

- Both the sender and recipient must be enrolled with Zelle® and have eligible U.S. bank accounts, limiting its use for international transactions.

ACH and Zelle Compared

Transaction Speed

ACH transactions typically take one to three business days to settle, as they are processed in batches at specific intervals. In contrast, Zelle offers real-time or near-real-time transfers, making it significantly faster for sending money between U.S. bank accounts. Lightspark further enhances speed by enabling instant, global money movement.

Fees

ACH transfers are generally low-cost, with fees ranging from $0.25 to $3, and sometimes free for account holders. Zelle transactions are usually free when conducted through participating banks. Lightspark also emphasizes low-cost transactions, reducing fees significantly for global payments.

Cross-Border Capabilities

ACH can handle some international transactions through International ACH Transfers (IAT), though it is primarily used for U.S. transactions. Zelle is limited to domestic transfers within the U.S. Lightspark excels in this area by offering seamless, low-cost, and reliable cross-border payments.

Security Protocols

ACH transfers are secure, benefiting from federal regulation and the ability to reverse transactions if fraud is detected. Zelle also employs secure messaging protocols and bank-level security measures. Lightspark leverages Bitcoin’s decentralized foundation, providing robust security through cryptographic protocols.

Operational Hours

ACH transactions are processed during specific intervals, often once or twice a day, with same-day processing available if requested before certain cut-off times. Zelle operates in real-time, implying 24/7 availability. Lightspark offers an "always on" infrastructure, enabling 24/7 global money movement.

How ACH And Zelle Are Used

Paying Monthly Bills

ACH is ideal for recurring monthly bills due to its ability to handle scheduled, automated payments. Zelle, while faster, lacks automation features. Lightspark offers real-time, low-cost payments, making it superior for both scheduled and instant bill payments globally.

Sending Money to Friends

Zelle excels in quick, informal transfers between friends, offering near-instantaneous transactions. ACH is slower but reliable for larger sums. Lightspark combines speed and low cost, enabling instant, secure transfers across borders, making it ideal for international peer-to-peer payments.

Business-to-Business Payments

ACH is commonly used for B2B transactions due to its batch processing and low fees. Zelle is less suitable for business payments. Lightspark provides instant, low-cost, and compliant solutions, making it advantageous for global B2B transactions.

International Remittances

ACH can handle international transfers but is slow and costly. Zelle is limited to domestic transactions. Lightspark's global reach and low-cost structure make it the best option for instant, secure international remittances.

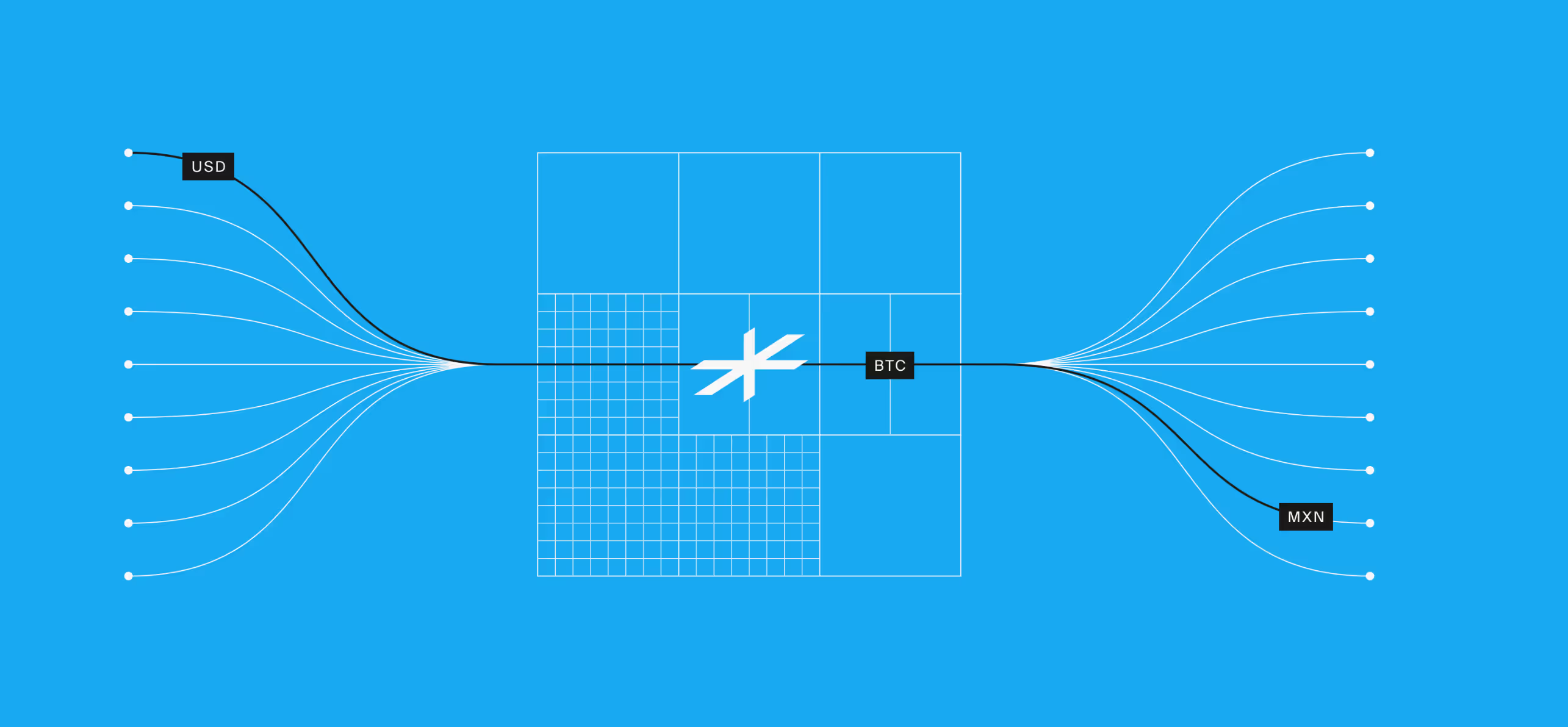

Time for a New Standard

Lightspark is a global payments platform that leverages Bitcoin’s decentralized foundation to offer real-time, low-cost, and secure cross-border money movement, surpassing the limitations of ACH and Zelle.

- Built on Bitcoin: Lightspark’s infrastructure is powered by Bitcoin and the Lightning Network, enabling instant, secure, and low-cost payments.

- Instant Settlement: The platform allows for immediate transfer and settlement of payments, both domestically and internationally.

- Lower fees: Lightspark offers transactions at a fraction of today’s costs, eliminating hidden fees and reducing the expense of cross-border and domestic payments.

- Cross-border security by default: Designed for secure, compliant-ready cross-border payments, Lightspark leverages Bitcoin’s decentralized network for inherent transaction security.

A Modern Infrastructure

For businesses looking to transcend traditional payment systems like ACH and Zelle, Lightspark offers the following solutions:

- Wallets: Build feature-rich digital wallets with flexible custody options, supporting Bitcoin, Lightning, stablecoins, and domestic payment rails.

- Digital Banks: Connect to the Money Grid to expand into new markets, move money 24/7, and stay competitive with real-time, global payments.

- Exchanges: Enable instant Bitcoin transfers, lower transaction costs, and built-in compliance tools for cryptocurrency exchanges.

- Stablecoins: Use Spark to create, distribute, and monetize stablecoins on the Bitcoin network, offering fast and cheap payments.

Emerging technologies and evolving regulations are reshaping the future of payments, making real-time, low-cost global transactions a reality. Lightspark leverages Bitcoin’s decentralized foundation to offer these advancements. Don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Learn more or book a demo.