Payment rails are the infrastructure that enables the transfer of money between banks, financial institutions, and payment service providers. For businesses, selecting the appropriate payment rail hinges on factors such as speed, cost, geography, and customer satisfaction.

ACH (Automated Clearing House) and CHIPS (Clearing House Interbank Payments System) are traditional payment rails that facilitate electronic funds transfers. However, Lightspark aims to transcend these systems by introducing a new category of global, real-time payments infrastructure.

The Payment Rail Landscape

Payment rails are crucial for moving money between parties, but current systems can be slow, fragmented, and costly, often leading to delays and higher transaction fees that impact both businesses and consumers.

Understanding ACH and CHIPS

How ACH Works

The Automated Clearing House (ACH) is an electronic funds-transfer system managed by Nacha. It processes large volumes of credit and debit transactions by batching them together and handling them at specific intervals. An ACH transaction starts when an originator initiates a direct deposit or payment. The originator's bank (ODFI) collects and batches these transactions, sending them to the ACH operator (Federal Reserve or a clearinghouse). The operator sorts and forwards them to the recipient's bank (RDFI), which then credits or debits the recipient's account. This process, facilitated by batch processing technology, can now often be completed on the same business day.

Strengths and Limitations of ACH

Strengths

- Makes online transactions quick and easy by batching and processing them at specific intervals throughout the day.

- Cost-effective, with low per-transaction fees, making it suitable for high-volume, low-value transactions.

- Versatile, supporting a wide range of transaction types including payroll, tax refunds, and bill payments.

Limitations

- Settlement can take up to three days, which is slower compared to real-time payment systems.

- Not suitable for high-value, time-sensitive transactions due to its batch processing nature.

- Limited to U.S. accounts, with international transactions only possible through specific bilateral agreements.

How CHIPS Works

CHIPS operates as an electronic payment system for large-value transactions, using multilateral netting to aggregate and offset payment obligations among participants. Transactions are queued and processed from 9 p.m. to 6 p.m. ET. The system involves two main steps: clearing (transfer and confirmation of information) and settlement (actual transfer of funds). CHIPS is a private sector real-time gross settlement system designed for efficiency, security, and reliability. A typical transaction flow includes transmitting a payment order, queuing, netting obligations, and final settlement, which is irrevocable and unconditional, ensuring the payer's obligation is fully discharged.

Strengths and Limitations of CHIPS

Strengths

- CHIPS is cost-effective, with lower fees compared to systems like Fedwire due to its netting mechanism.

- It ensures secure and timely settlements for high-value interbank transfers, corporate payments, and other financial transactions.

- CHIPS supports a wide range of payment types, including interbank transfers, corporate payments, foreign exchange transactions, and government payments.

Limitations

- CHIPS is slower than Fedwire, as it does not provide real-time settlement for all transactions.

- It operates only during specific hours (9 p.m. to 6 p.m. ET), limiting its availability for urgent transactions outside these times.

- CHIPS is primarily designed for large-value transactions and is not suitable for retail payments or low-value transactions.

ACH and CHIPS Compared

Transaction Speed

ACH transactions typically take 1-3 business days to settle, though same-day ACH is available for an additional fee. CHIPS offers same-day settlement, making it faster for high-value transactions. In contrast, Lightspark provides real-time, instant money movement, ensuring transactions are completed without delays.

Fees

ACH is cost-effective, with low per-transaction fees, often less than a cent for banks and up to a few cents for payment processors. CHIPS has higher per-transaction fees but benefits from netting efficiency, making it cheaper than Fedwire for high-value transactions. Lightspark emphasizes low-cost transactions, moving money at a fraction of today's costs.

Cross-Border Capabilities

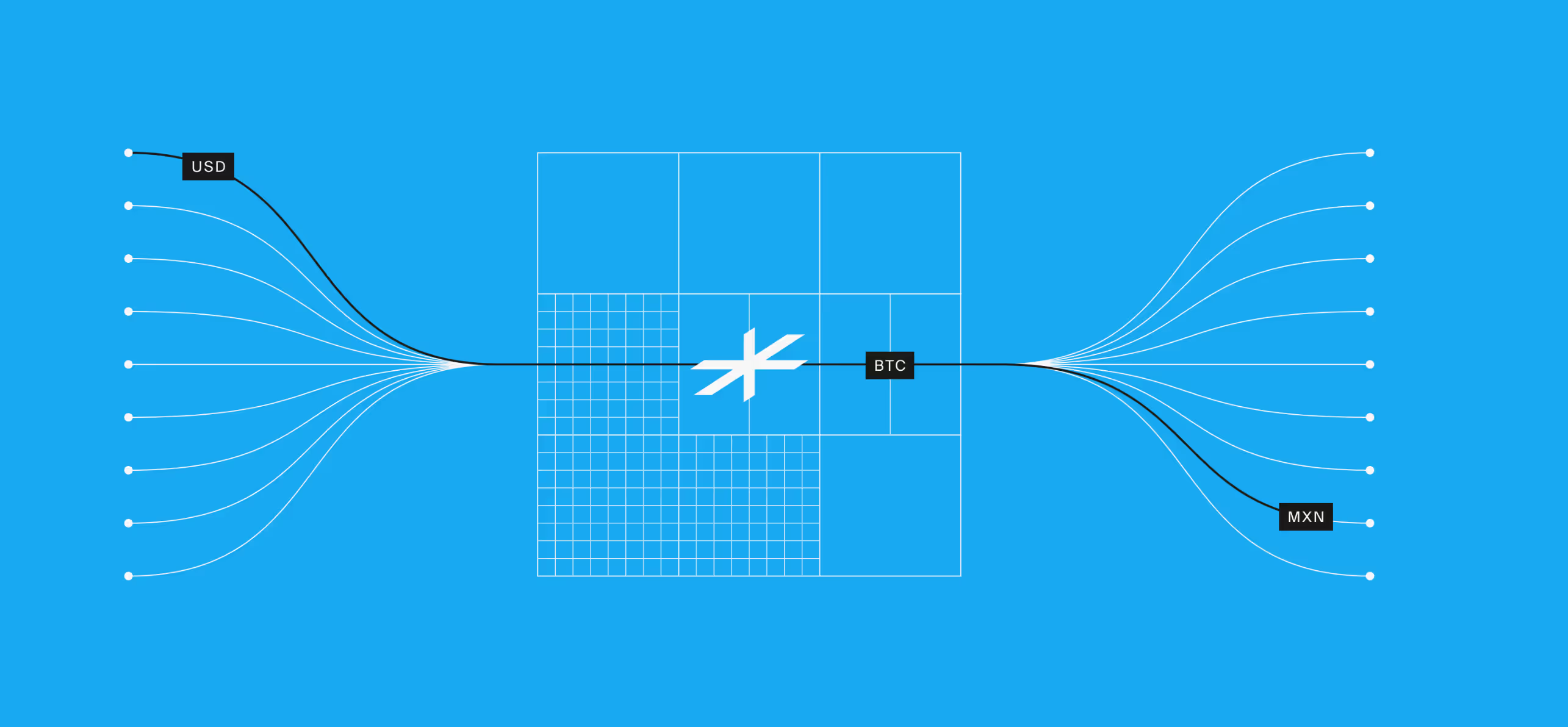

ACH is primarily a domestic payment system, limited to the U.S. with few bilateral agreements for international transactions. CHIPS supports large-value international USD payments, making it suitable for cross-border transactions. Lightspark excels in global reach, supporting payments in 94+ countries and 75+ currencies.

Security Protocols

ACH transactions are governed by Nacha, ensuring safety and compliance, though specific security measures are not detailed. CHIPS employs multi-layered authentication, encryption, and monitoring systems for high-value transfers. Lightspark leverages Bitcoin’s decentralized foundation, providing robust security through blockchain technology.

Operational Hours

ACH processes transactions in batches with multiple daily windows but does not operate 24/7. CHIPS operates from 9 a.m. to 6 p.m. ET on U.S. business days. Lightspark offers 24/7 availability, enabling continuous, real-time payments without the constraints of traditional banking hours.

How ACH And CHIPS Are Used

Payroll Processing

ACH is ideal for payroll due to its low cost and support for recurring payments, though it may take up to three days to settle. CHIPS is less suitable due to higher fees and focus on high-value transactions. Lightspark offers instant, low-cost payroll processing, ensuring employees are paid in real-time.

Supplier Payments

ACH is commonly used for supplier payments, offering cost efficiency but slower settlement times. CHIPS can handle large payments but is more expensive. Lightspark enables instant, secure payments, reducing delays and improving cash flow for suppliers.

International Transactions

CHIPS supports large-value international payments but is limited by operating hours and higher fees. ACH is generally unsuitable for cross-border transactions. Lightspark excels with 24/7 global reach, supporting multiple currencies and providing real-time settlement.

High-Value Corporate Payments

CHIPS is designed for high-value corporate payments, offering same-day settlement but at a higher cost. ACH is not suitable due to its batch processing and lower transaction limits. Lightspark provides instant, low-cost transfers, enhancing efficiency and reducing operational costs for corporations.

Time for a New Standard

Lightspark is a global payments infrastructure provider that offers real-time, cross-border money movement for Bitcoin, fiat, and stablecoins, surpassing the limitations of ACH and CHIPS with its instant, secure, and low-cost payment solutions.

- Built on Bitcoin: Lightspark’s infrastructure leverages Bitcoin’s open, decentralized foundation, enabling a global payments network that bridges traditional financial systems with next-generation technology.

- Instant Settlement: The platform ensures real-time, instant settlement of payments, making money move like information on the Internet—instantly, securely, and at a fraction of today’s costs.

- Lower fees: Lightspark offers low-cost transactions, reducing float and eliminating hidden fees, making it a cost-effective alternative to traditional payment rails.

- Cross-border security by default: Designed for secure, cross-border payments, Lightspark combines current financial infrastructure with new technology, ensuring seamless, low-cost, and reliable payments across borders.

A Modern Infrastructure

For businesses looking to transcend the limitations of legacy payment systems like ACH and CHIPS, Lightspark offers the following solutions:

- Wallets: Build feature-rich wallets with flexible custody options, supporting Bitcoin, Lightning, stablecoins, and domestic payment rails.

- Digital Banks: Connect to the 'Money Grid' to expand into new markets, move money 24/7, and stay competitive with real-time, low-cost payments.

- Exchanges: Enable instant, low-cost Bitcoin transfers and integrate seamlessly with the Lightning Network for faster, more efficient transactions.

- Stablecoins: Use Spark to create, distribute, and monetize stablecoins on Bitcoin, offering a fast, cheap, and user-friendly way to build financial applications.

Emerging technologies and evolving regulations are reshaping the future of payments. Lightspark can help businesses achieve real-time, low-cost global payments. Don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Learn more or book a demo.