Payment rails are the digital networks that facilitate fund transfers between financial institutions. For any enterprise, selecting the optimal rail involves weighing variables such as transaction velocity, operational expense, geographic reach, and end-user experience. Common examples include Automated Clearing House (ACH) for batch processing and Real-Time Gross Settlement (RTGS) for high-value, instant transfers.

In response to the limitations of these legacy systems, companies like Lightspark are pioneering a new category of payments infrastructure. They aim to move beyond traditional rails by building on Bitcoin’s open, decentralized foundation for faster, lower-cost global transactions.

The Payment Rail Landscape

These networks are the fundamental highways for commerce, but the current landscape is a patchwork of systems. This fragmentation often leads to transactions that are slow to settle, burdened by high fees, and limited in their global reach.

Understanding ACH and RTGS

How ACH Works

The Automated Clearing House (ACH) is an electronic network for moving money between bank accounts in the U.S., managed by Nacha. It operates on a batch-processing system, where transactions are bundled together and processed at set times throughout the day. A typical transaction begins when an originator, like an employer, initiates a payment. Their bank collects these requests into a batch and sends it to an ACH operator, such as the Federal Reserve. The operator sorts the batch and forwards the individual transactions to the respective recipient banks, which then credit or debit the final accounts, completing the transfer.

Strengths and Limitations of ACH

Strengths

- ACH is highly cost-effective, often involving lower flat fees compared to the percentage-based costs of credit cards or the high fees of wire transfers.

- It is exceptionally convenient for handling recurring payments, making it ideal for payroll, direct deposits, and automated bill payments.

- The network is built to reliably process enormous volumes of transactions, handling billions of payments worth trillions of dollars each quarter.

Limitations

- Transactions are processed in batches rather than in real-time, which can result in settlement delays of several hours or even days.

- Financial institutions frequently impose transaction limits, restricting the maximum amount of money that can be transferred in a single payment.

- The system is not universally available in all countries, which can pose a challenge for businesses conducting global transactions.

How RTGS Works

Real-Time Gross Settlement (RTGS) is an electronic funds transfer system managed by central banks for high-value, urgent payments. Unlike batch processing, RTGS operates on a continuous basis. When a bank initiates a transfer, the instruction is sent to the central bank’s RTGS system, which processes it immediately and individually—this is the “gross settlement” aspect. The central bank electronically debits the sender’s account and credits the receiver’s. This settlement is instantaneous, final, and irrevocable, minimizing risk by ensuring funds are cleared and available in real-time without any netting of transactions.

Strengths and Limitations of RTGS

Strengths

- RTGS provides the fastest way of transferring money by settling transactions individually and in real-time.

- Payments are final and irrevocable once completed, which minimizes settlement risk by eliminating delays between interbank transactions.

- The system is ideal for high-value transactions, such as large corporate payments and interbank transfers, due to its high transaction limits.

Limitations

- RTGS transactions are generally more expensive than other payment systems, with banks charging a fee for each transfer.

- The system is often unsuitable for small-value payments, as some jurisdictions impose a minimum transaction amount.

- Transfers can be subject to numerous conditions by the central bank that complicate the process for users.

ACH and RTGS Compared

Transaction Speed

RTGS offers near-instant settlement for individual transactions, while ACH processes payments in batches, leading to delays of hours or even days. In contrast, modern solutions built on the Lightning Network are designed for truly real-time, global payments that move like information online.

Fees

ACH is a cost-effective option with low, often flat fees, making it ideal for recurring payments. RTGS is significantly more expensive due to its complex, real-time infrastructure. Next-generation networks like Lightspark aim to reduce these costs to a fraction of traditional fees.

Cross-Border Capabilities

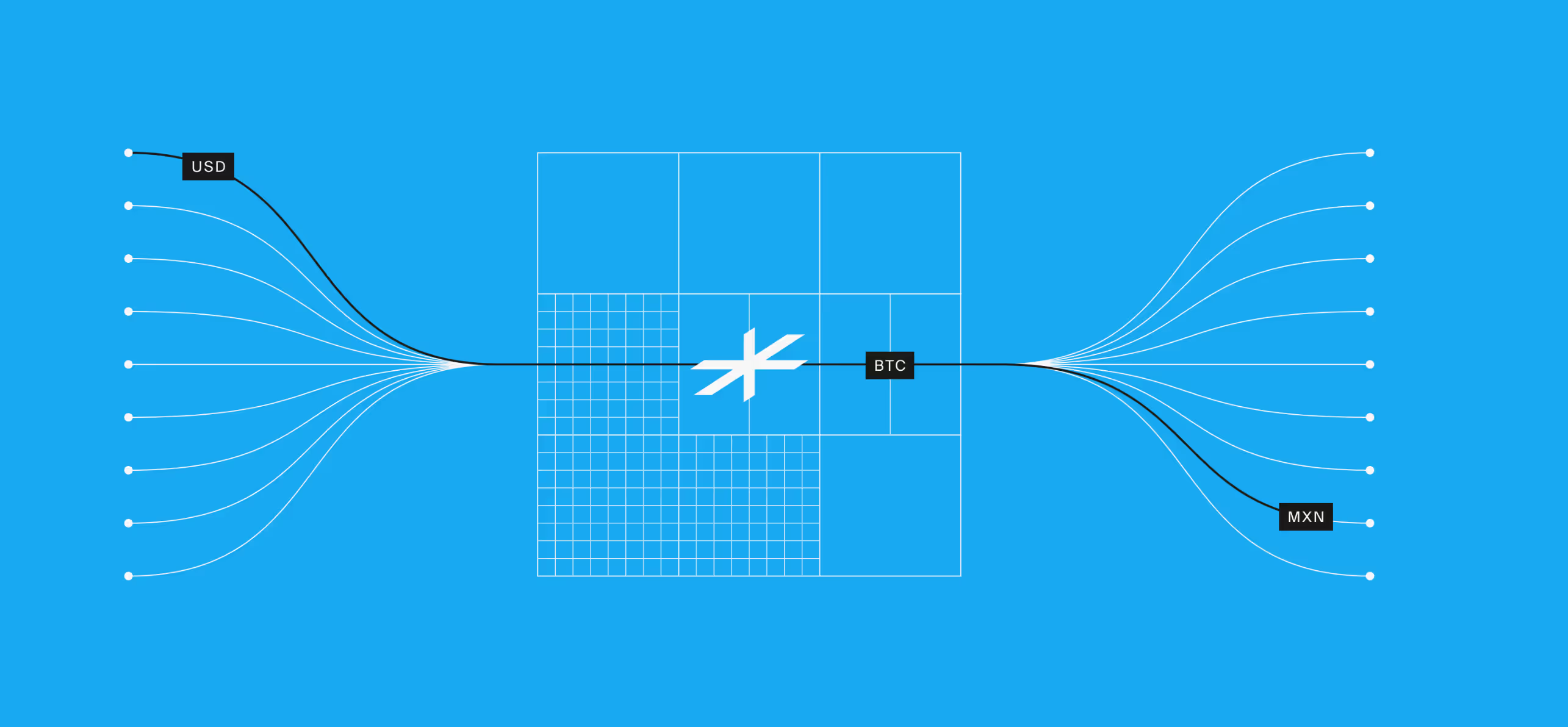

Both ACH and RTGS are typically designed for domestic transfers within a single country, limiting their use for international business. This stands in contrast to open, global networks like Lightspark, which are built specifically for seamless cross-border payments across dozens of countries.

Security Protocols

Both systems are highly secure; ACH operates under strict regulations, while RTGS uses advanced encryption for high-value transfers. Modern payment infrastructures like Lightspark introduce a different security model, leveraging the decentralized, cryptographic security inherent in Bitcoin’s open-source foundation.

Operational Hours

ACH operates on a schedule tied to business days, processing transactions in batches at specific times. While RTGS is often available 24/7, next-generation platforms like Lightspark are inherently “always on,” enabling continuous, uninterrupted payment flows without reliance on traditional banking hours.

How ACH And RTGS Are Used

Payroll and Direct Deposits

For recurring payments like salaries, ACH is typically preferred over the more expensive RTGS system due to its cost-effectiveness for bulk transfers. Lightspark enhances this by enabling instant, 24/7 payroll settlement, eliminating the multi-day processing delays common with ACH and giving employees immediate access to their funds.

High-Value Corporate Payments

RTGS is the standard for large, urgent corporate payments, offering immediate and irrevocable settlement where ACH is unsuitable due to transaction limits. For global enterprises, Lightspark’s Money Grid offers a superior alternative, facilitating instant, low-cost cross-border payments without the high fees and delays of traditional international wires.

Cross-Border Commerce

Traditional rails like ACH and RTGS are largely domestic, making international commerce slow and expensive. Lightspark is built for this scenario, enabling businesses to expand into new corridors and settle in local currencies instantly, bypassing the gatekeepers, delays, and hidden fees inherent in legacy systems.

Digital Wallet and Exchange Transfers

Exchanges and wallets often rely on slow ACH transfers for user payouts. Lightspark provides a significant upgrade with instant, low-cost Bitcoin transfers, handling complex liquidity and routing to ensure seamless interoperability and a better user experience for customers moving funds globally.

Time for a New Standard

Lightspark provides a modern payments infrastructure built on Bitcoin’s open foundation, enabling real-time global money movement that bypasses the slow, costly, and fragmented nature of traditional systems like ACH and RTGS. It offers a superior alternative by connecting businesses to a network where money moves instantly and securely at a fraction of the cost.

- Built on Bitcoin: The platform's core network is built on Bitcoin’s open, decentralized foundation, leveraging its technology for secure and innovative payment solutions.

- Instant Settlement: Lightspark enables real-time, 24/7 payments, ensuring that funds are settled instantly across borders without the delays common in legacy systems.

- Lower fees: By design, the network facilitates payments at a fraction of traditional costs, eliminating hidden fees and reducing the financial burden of transactions.

- Cross-border security by default: The infrastructure is built for secure international payments, leveraging Bitcoin’s decentralized security model to ensure compliant and reliable transfers globally.

A Modern Infrastructure

For businesses ready to advance beyond legacy payment rails like ACH and RTGS, Lightspark delivers a suite of powerful solutions:

- Wallets: Enables businesses to build feature-rich digital wallets with flexible custody, providing real-time access to Bitcoin, the Lightning Network, and stablecoins.

- Digital Banks: Connects digital banks to a global money network, helping them expand into new markets and move money 24/7 with lower transaction costs.

- Exchanges: Allows cryptocurrency exchanges to seamlessly connect to the Bitcoin Network, facilitating instant, low-cost Bitcoin transfers for their customers.

- Stablecoins: Through its Spark platform, businesses can create, distribute, and monetize their own stablecoins natively on the Bitcoin network.

The future of payments is being shaped by emerging technologies and evolving regulations. Don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Lightspark enables real-time, low-cost global payments, helping you move beyond legacy systems. To see how it works, learn more or book a demo.