Payment rails are the infrastructure that enables the transfer of money between banks, financial institutions, and other entities. For businesses, selecting the appropriate payment rail hinges on factors such as transaction speed, cost, geographical reach, and customer satisfaction.

CHAPS and SWIFT are two prominent examples of traditional payment rails. CHAPS is a UK-based system for high-value transactions, while SWIFT facilitates international payments. Lightspark aims to transcend these systems by introducing a new global payments network that leverages Bitcoin’s decentralized foundation.

The Payment Rail Landscape

Payment rails are crucial for moving money between parties, but current systems can be slow, fragmented, and costly, often leading to inefficiencies and higher expenses for businesses and consumers alike.

Understanding CHAPS and SWIFT

How CHAPS Works

CHAPS (Clearing House Automated Payment System) is a sterling same-day system for high-value and time-critical payments. It operates using the Bank of England's Real-Time Gross Settlement (RTGS) infrastructure and the SWIFT messaging network. Payments are settled individually and irrevocably on a gross basis in real time. The process involves direct participants submitting payment obligations via SWIFT, which are then settled in RTGS. Indirect participants access CHAPS through direct participants. The system is open from 6am to 6pm on working days, ensuring secure and efficient transactions with no minimum or maximum payment limit.

Strengths and Limitations of CHAPS

Strengths

- CHAPS provides same-day settlement for high-value and time-critical payments, ensuring funds are transferred quickly and efficiently within the UK.

- The system operates with high operational resilience, leveraging the Bank of England’s RTGS infrastructure and the SWIFT messaging network.

- There are no minimum or maximum payment limits, making it suitable for a wide range of transaction sizes.

Limitations

- CHAPS involves significant costs, including one-off setup fees and ongoing charges, making it less suitable for smaller, routine transactions.

- The system is limited to UK sterling payments and is not available for international transactions.

- Joining as a direct participant can be a lengthy process, typically taking twelve to eighteen months.

How SWIFT Works

SWIFT operates as a global member-owned cooperative, connecting over 11,000 financial institutions to facilitate secure, standardized financial messaging. It does not hold funds but provides a platform for exchanging financial messages. Transactions involve creating standardized messages (e.g., ISO 20022) that are securely transmitted via SWIFT’s network to recipient institutions identified by BIC codes. SWIFT’s technology stack includes secure messaging platforms, integration interfaces, and cloud-based solutions, ensuring reliability and compliance. Tools like Swift GPI enhance transaction speed and transparency, while the Customer Security Programme fortifies cybersecurity.

Strengths and Limitations of SWIFT

Strengths

- SWIFT has a global reach, connecting over 11,000 financial institutions in more than 200 countries, facilitating international payments.

- It offers extensive currency support, allowing transactions in multiple currencies such as USD, EUR, and GBP.

- SWIFT ensures secure and reliable financial messaging with robust anti-fraud checks and compliance measures.

Limitations

- SWIFT payments can be slow, taking 1-4 business days to process due to intermediary banks and compliance checks.

- The system involves high fees, often ranging from €10-50 to send and €5-20 to receive, with additional costs for intermediary banks.

- SWIFT requires detailed recipient and bank information, adding complexity to the transaction process.

CHAPS and SWIFT Compared

Transaction Speed

CHAPS offers same-day settlement for high-value payments within the UK, ensuring funds are transferred quickly and efficiently. In contrast, SWIFT transactions can take 1-4 business days due to intermediary banks and compliance checks. Lightspark, leveraging the Lightning Network, provides real-time, instant money movement, surpassing both CHAPS and SWIFT in speed.

Fees

CHAPS transactions typically incur fees ranging from £25-£35, making it costly for smaller, routine payments. SWIFT fees are higher, often costing €10-50 to send and €5-20 to receive, with additional charges for intermediary banks. Lightspark emphasizes low-cost payments, offering a more economical alternative for global transactions.

Cross-Border Capabilities

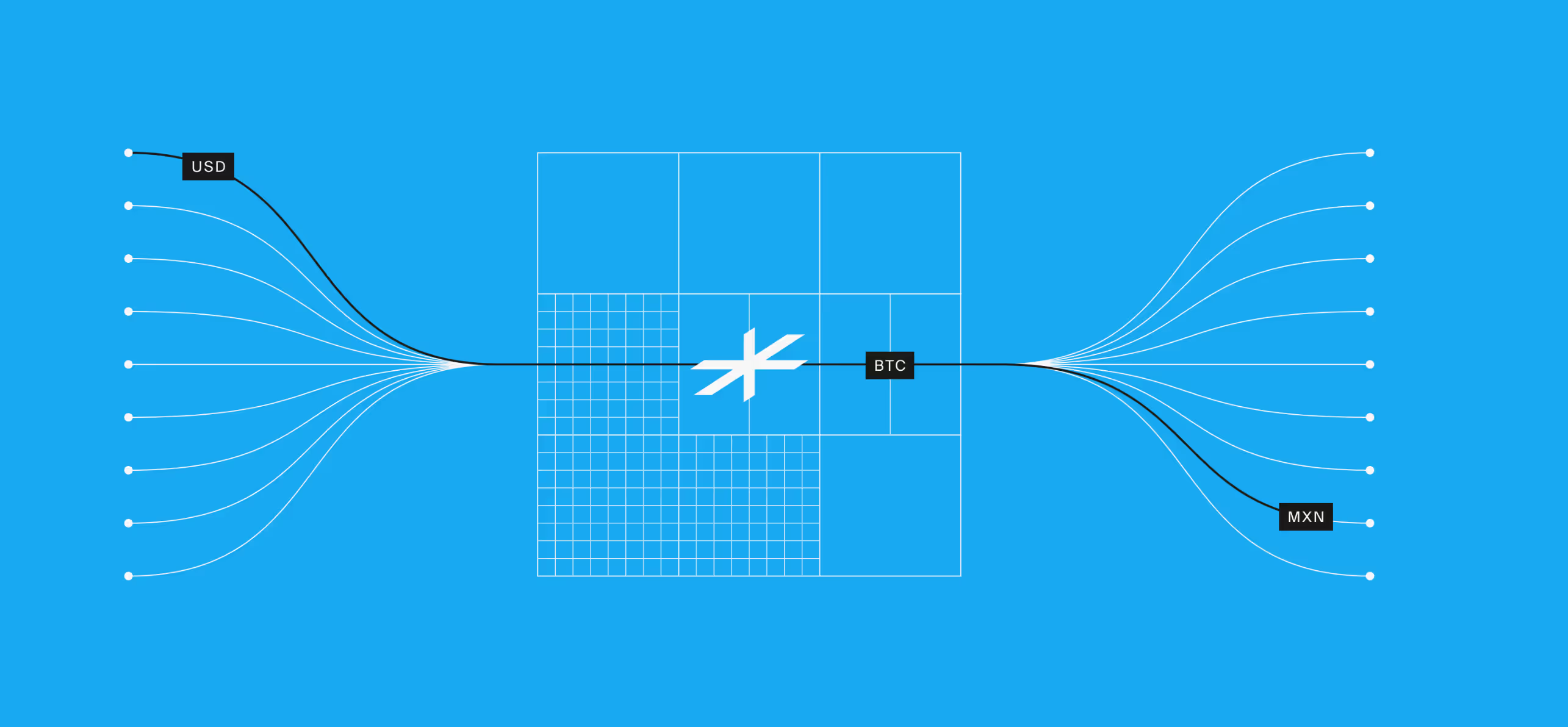

CHAPS is limited to domestic UK transactions and does not support cross-border payments. SWIFT, however, facilitates international payments, connecting over 11,000 financial institutions in more than 200 countries. Lightspark excels in cross-border capabilities, enabling seamless, low-cost payments across 94+ countries.

Security Protocols

CHAPS ensures secure transactions through the Bank of England’s RTGS infrastructure, while SWIFT employs robust anti-fraud checks and compliance measures. Although both systems are secure, Lightspark offers enhanced security by leveraging Bitcoin’s decentralized foundation and the Lightning Network’s built-in compliance features.

Operational Hours

CHAPS operates on business days with specific cutoff times, while SWIFT’s operational hours vary by institution, often leading to delays. Lightspark, on the other hand, provides 24/7 operational capability, ensuring payments can be processed at any time, anywhere.

How CHAPS And SWIFT Are Used

High-Value Domestic Payments

CHAPS is ideal for urgent, high-value payments within the UK, such as property purchases, due to its same-day settlement. SWIFT is not suitable for these transactions as it is slower and more costly. Lightspark offers instant, low-cost payments, making it a superior choice for high-value domestic transactions.

International Supplier Payments

SWIFT is commonly used for paying international suppliers, offering secure cross-border transactions. However, it can be slow and expensive. Lightspark provides real-time, low-cost global payments, making it a more efficient option for international supplier payments.

Cross-Border Business Transactions

SWIFT facilitates international business transactions but involves high fees and delays. CHAPS is not applicable for cross-border payments. Lightspark excels in this scenario by enabling instant, low-cost payments across 94+ countries, enhancing operational efficiency for businesses.

Urgent Personal Transfers

CHAPS is suitable for urgent, high-value personal transfers within the UK, such as settling large invoices. SWIFT is less ideal due to slower processing times. Lightspark offers instant, secure transfers, making it a better alternative for urgent personal payments.

Time for a New Standard

Lightspark offers a global payments infrastructure that leverages Bitcoin’s decentralized foundation to provide real-time, low-cost, and secure money movement, surpassing the limitations of CHAPS and SWIFT.

- Built on Bitcoin: Lightspark’s infrastructure is powered by Bitcoin, enabling instant, secure, and low-cost money movement.

- Instant Settlement: The platform allows for real-time, global money movement for Bitcoin, fiat, and stablecoins.

- Lower Fees: Lightspark emphasizes low-cost payments, reducing the need for intermediaries and associated costs.

- Cross-Border Security by Default: Built on Bitcoin’s open, decentralized, and secure foundation, Lightspark ensures strong security for cross-border payments.

A Modern Infrastructure

For businesses looking to transcend traditional payment systems like CHAPS and SWIFT, Lightspark offers the following solutions:

- Wallets: Build advanced digital wallets with flexible custody options, supporting Bitcoin, Lightning Network, stablecoins, and domestic payment rails.

- Digital Banks: Connect to the Money Grid to expand into new markets, offer 24/7 payments, and stay competitive with real-time, low-cost transactions.

- Exchanges: Seamlessly integrate with the Bitcoin Network to enable instant, low-cost bitcoin transfers, enhancing user experience and reducing operational costs.

- Stablecoins: Use Spark to create, distribute, and monetize stablecoins on the Bitcoin network, offering fast, cheap, and user-friendly financial applications.

Emerging technologies and evolving regulations are reshaping the future of payments, making it essential to upgrade to a payment rail built for the internet age. Lightspark can help achieve real-time, low-cost global payments. Learn more or book a demo to stay ahead.