Payment rails are the digital networks facilitating money transfers between financial institutions. For any enterprise, selecting an appropriate rail involves weighing variables like transaction velocity, operational expense, geographic reach, and end-user experience. Prominent examples include the SWIFT network for interbank messaging and Western Union for global remittances.

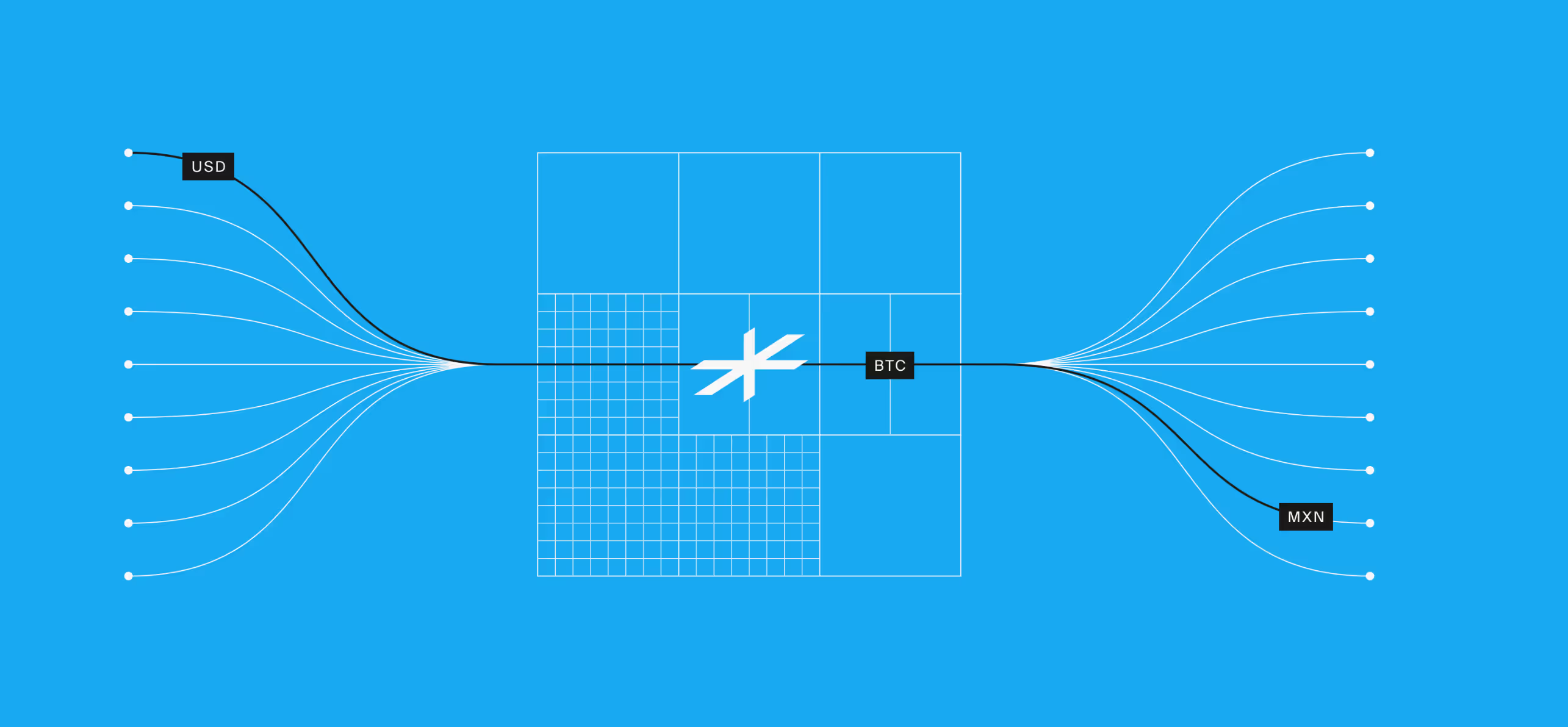

In contrast, Lightspark is pioneering a new category of payments infrastructure. It leverages Bitcoin’s open, decentralized foundation to build a “Money Grid” for real-time, low-cost money movement, aiming to bypass the limitations of legacy systems.

The Payment Rail Landscape

Payment rails are the essential infrastructure for moving money. However, today's systems are often a patchwork of slow, disconnected networks, leading to high fees and delays for businesses and consumers alike.

Understanding SWIFT and Western Union

How SWIFT Works

The Society for Worldwide Interbank Financial Telecommunication (SWIFT) operates as a global cooperative providing secure financial messaging services that connect over 11,000 institutions. It doesn't move money itself but provides the network for transmitting transaction information. The process involves institutions connecting their back-office systems to SWIFT's network using technologies like Alliance Cloud. To initiate a transaction, a standardized message, often formatted with the ISO 20022 standard, is created and sent securely. The recipient institution then processes this message to complete the transaction, with SWIFT providing tools for tracking, validation, and compliance throughout the flow.

Strengths and Limitations of SWIFT

Strengths

- With a network connecting over 11,000 institutions in more than 200 countries, SWIFT offers unparalleled global reach for international financial transactions.

- The system provides highly secure and reliable messaging using standardized formats, which ensures payments are routed accurately between financial institutions worldwide.

- SWIFT supports a comprehensive suite of services, including risk management, compliance analytics, and leadership in adopting new standards like ISO 20022.

Limitations

- International transfers using SWIFT can be expensive and slower compared to modern fintech alternatives due to intermediary bank fees and processing times.

- The system is operationally complex, requiring extensive information for each transaction and significant compliance overhead for member institutions.

- A SWIFT code only identifies a bank and branch, not an individual's account, necessitating additional information like an IBAN to avoid payment delays or failures.

How Western Union Works

Western Union operates as a global money transfer service, allowing users to send funds online, via its app, or in person at an agent location. Recipients can receive the money as a direct bank deposit or collect it in cash. The process begins with the sender registering an account and providing the recipient’s details. After choosing a payment method, such as a credit card or bank transfer, the system generates a unique Money Transfer Control Number (MTCN). This number is essential for tracking the transaction and is required, along with a valid ID, for the recipient to pick up cash.

Strengths and Limitations of Western Union

Strengths

- Its vast global network of physical agent locations makes it highly accessible for sending and receiving cash worldwide.

- It offers multiple sending and receiving options, including online, via an app, or in-person, with recipients able to get funds via bank deposit or cash pickup.

- The service provides rapid transfer options, allowing funds to be available for cash pickup in just a few minutes.

Limitations

- Western Union often charges significant fees and adds a markup to the mid-market exchange rate, making transfers more expensive than they appear.

- The service is not intended for online shopping and offers limited buyer or seller protection, increasing the risk for commercial transactions.

- For international transfers, its combination of fees and less competitive exchange rates can make it a less economical choice compared to newer fintech startups.

SWIFT and Western Union Compared

Transaction Speed

SWIFT transfers can take several business days to clear due to intermediary bank processing. Western Union offers faster options, including next-day service and near-instant transfers that can be completed in a matter of minutes. In contrast, platforms like Lightspark are built for instant, real-time payments, aiming to eliminate delays entirely.

Fees

SWIFT transactions incur fees from sending, intermediary, and receiving banks, with international wires costing around $45. Western Union charges transfer fees and also builds costs into its exchange rates. Newer infrastructures like Lightspark focus on providing low-cost payments with no hidden fees, reducing transaction expenses.

Cross-Border Capabilities

Both systems offer extensive global reach. SWIFT connects financial institutions in over 200 countries, while Western Union facilitates international remittances to a wide range of destinations. Similarly, emerging platforms like Lightspark are building global payment networks to connect dozens of countries and currencies for seamless cross-border transactions.

Security Protocols

SWIFT relies on standardized, secure messaging to ensure transactional integrity across its network. Western Union is considered a dependable service for transfers. Modern solutions like Lightspark leverage the inherent security of decentralized foundations like Bitcoin, while also incorporating built-in compliance features.

Operational Hours

SWIFT transfer processing is often tied to traditional banking hours and cut-off times. Western Union offers 24/7 online services, but cash transactions are limited by agent hours. In contrast, networks like Lightspark are designed to be always on, enabling 24/7 payments.

How SWIFT And Western Union Are Used

International Trade Finance

For large, secure B2B payments, SWIFT is generally more suitable than Western Union due to its established bank-to-bank framework. Lightspark enhances this by enabling instant, low-cost global settlements on its Money Grid, reducing operational float and bypassing the delays and high fees of traditional rails.

Personal Remittances

Western Union is often preferred for sending cash to family, especially when the recipient lacks a bank account or needs funds quickly. For the digitally connected, Lightspark offers a superior alternative, facilitating instant, low-fee transfers directly to wallets and avoiding the high costs of legacy remittance services.

Paying Global Contractors

While SWIFT offers a formal payment channel for international contractors, its slowness and cost are notable drawbacks. Lightspark’s real-time payment network allows businesses to settle invoices instantly and cheaply across borders, improving contractor satisfaction and streamlining payroll operations without the usual cross-border friction.

Cross-Border E-commerce Payouts

E-commerce platforms often use SWIFT for seller payouts, but this process can be slow. Lightspark’s infrastructure is ideal for this scenario, enabling instant, scalable, and low-cost payouts to a global seller base, which enhances a platform’s value by ensuring sellers receive their funds immediately.

Time for a New Standard

Unlike the slow and costly networks of SWIFT and Western Union, Lightspark provides a modern payments infrastructure built on Bitcoin, enabling instant, low-cost, and open money movement across the globe.

- Built on Bitcoin: Lightspark’s infrastructure is built on Bitcoin’s open, decentralized foundation, using its Money Grid and the Lightning Network to power a global payments network.

- Instant Settlement: The platform is designed for real-time, global money movement, enabling 24/7 payments that settle instantly, much like information on the internet.

- Lower Fees: By removing gatekeepers and hidden charges, Lightspark facilitates payments at a fraction of the cost of traditional systems, making cross-border transactions more affordable.

- Cross-Border Security by Default: Leveraging Bitcoin’s decentralized foundation, the network provides inherently secure and reliable cross-border payments, with compliance features built directly into the infrastructure.

A Modern Infrastructure

For businesses looking to transcend the limitations of legacy payment rails, Lightspark provides a suite of modern solutions:

- Wallets: Enables businesses and developers to build feature-rich digital wallets with flexible custody options at scale, supporting Bitcoin, Lightning, and stablecoins.

- Digital Banks: Offers a comprehensive solution for digital banks to connect to the 'Money Grid,' a global, open money network for rapid market expansion and 24/7 payments.

- Exchanges: Provides the easiest way for cryptocurrency exchanges to connect to the Bitcoin Network and power instant, low-cost bitcoin movement.

- Stablecoins: Through Spark, businesses can create, distribute, and monetize their own stablecoins on the Bitcoin network in minutes.

Emerging technologies like Bitcoin and stablecoins, guided by evolving regulations, are defining the future of payments. Don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Lightspark enables real-time, low-cost global payments. Learn more or book a demo to modernize your infrastructure.