Payment rails are the infrastructure that enables the transfer of money between banks, payment service providers, and other financial institutions. For businesses, choosing the right payment rail depends on factors like speed, cost, geography, and customer satisfaction.

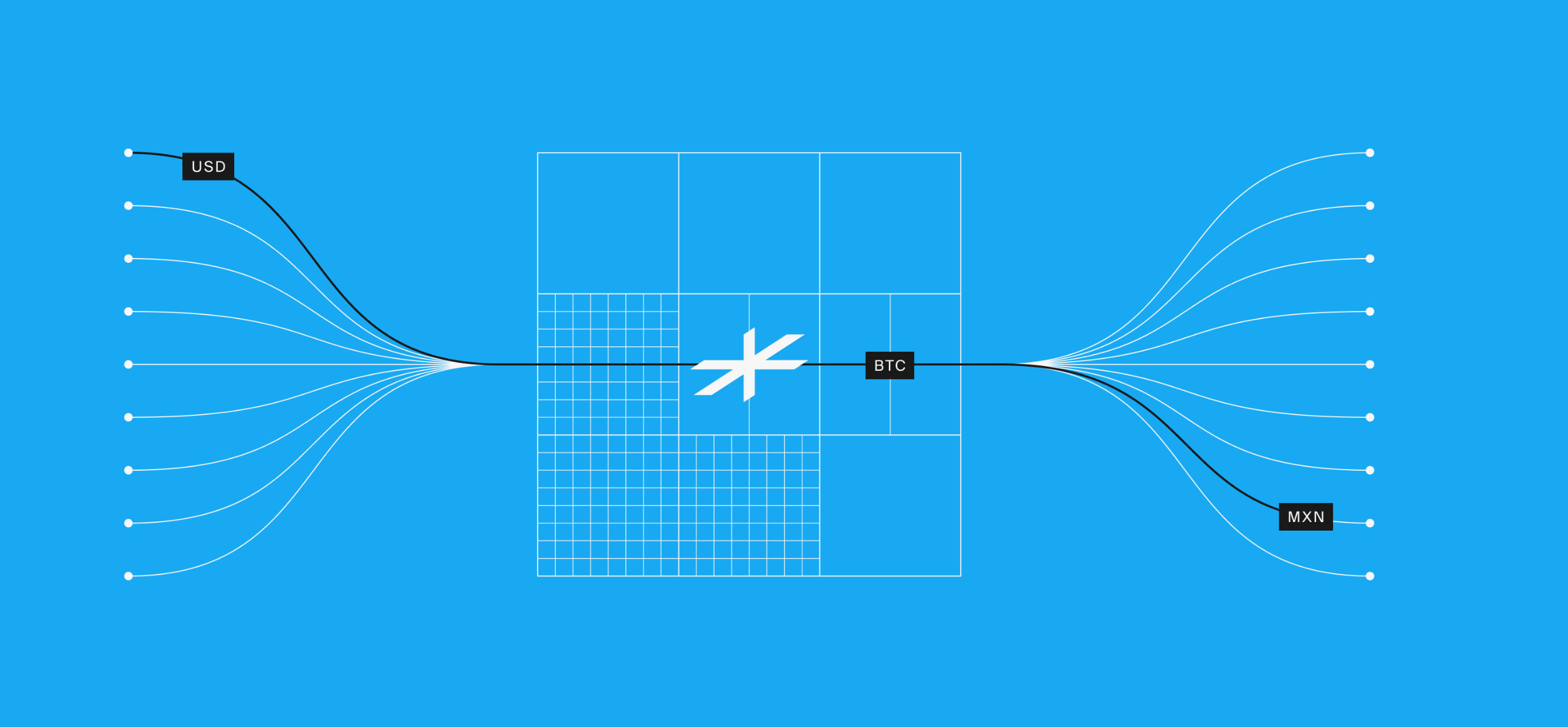

ACH and SWIFT are two widely used payment rails. ACH is primarily used for domestic transactions in the United States, offering low-cost and reliable transfers. SWIFT, on the other hand, facilitates international payments, connecting banks across the globe. Lightspark aims to move past these traditional rails by introducing a new, open global payments network built on Bitcoin’s decentralized foundation.

The Payment Rail Landscape

Payment rails are crucial for moving money between parties, but current systems can be slow, fragmented, and costly, often leading to delays and higher fees for businesses and consumers alike.

Understanding ACH and SWIFT

How ACH Works

The Automated Clearing House (ACH) is an electronic funds-transfer system managed by Nacha. It processes large volumes of credit and debit transactions by batching them together and processing at specific intervals. An ACH transaction starts when an originator initiates a direct deposit or payment. The originator's bank (ODFI) collects and batches these requests, sending them to the ACH operator (Federal Reserve or a clearinghouse). The operator sorts and distributes the transactions to the recipient's bank (RDFI), which then credits or debits the recipient's account. The process is completed when both accounts are reconciled, with same-day settlement available for most transactions.

Strengths and Limitations of ACH

Strengths

- Makes online transactions quick and easy by batching and processing them at specific intervals throughout the day.

- Offers low-cost transactions, typically less than $1 per transaction, making it cost-effective for high-volume payments.

- Provides same-day settlement for most transactions, enhancing efficiency and timeliness.

Limitations

- Some banks may impose transaction limits, requiring multiple transactions for larger amounts.

- ACH payments are primarily domestic, with limited international capabilities and support.

- Not all transactions are instant, with some taking one to two business days to settle.

How SWIFT Works

SWIFT operates as a global member-owned cooperative, connecting over 11,000 financial institutions to facilitate secure, standardized financial messaging. It does not hold funds but provides a platform for exchanging payment instructions and compliance information. Transactions begin with a financial institution using its back-office system, connected to SWIFT’s network via solutions like Alliance Cloud. Messages are formatted using standards like ISO 20022 and securely transmitted to the recipient institution. SWIFT’s technology stack includes tools for payment pre-validation, fraud control, and compliance analytics, ensuring secure, efficient, and transparent transactions.

Strengths and Limitations of SWIFT

Strengths

- SWIFT has a global reach, connecting over 11,000 financial institutions in more than 200 countries and territories, making it ideal for international payments.

- It provides secure and standardized communication, ensuring accurate and reliable transmission of payment instructions and transaction details.

- SWIFT payments can be fast, often settling within one to five business days, with some transactions completing in as little as 24 hours.

Limitations

- SWIFT transactions can be costly, with fees ranging from $20 to $50 per transaction, and additional fees possible if intermediary banks are involved.

- The exact amount received by the payee can be uncertain due to potential intermediary bank fees, making it difficult to predict the final settlement amount.

- Once a SWIFT payment is initiated, it is very difficult to stop or reverse, increasing the risk of error and fraud.

ACH and SWIFT Compared

Transaction Speed

ACH transactions typically take one to three business days to process, with options for same-day settlement. SWIFT payments generally settle within one to five business days, but can be delayed if intermediary banks are involved. Lightspark offers instant, real-time payments, significantly reducing transaction times.

Fees

ACH fees are low, usually less than $1 per transaction, making it cost-effective for high-volume payments. SWIFT transactions are more expensive, ranging from $20 to $50 per transaction, with additional fees possible. Lightspark provides low-cost payments, eliminating hidden fees and reducing overall transaction costs.

Cross-Border Capabilities

ACH is primarily for domestic transactions, with limited international capabilities through Global ACH. SWIFT excels in international payments, connecting over 11,000 financial institutions worldwide. Lightspark supports seamless, low-cost cross-border payments, leveraging Bitcoin’s decentralized network to bridge financial systems globally.

Security Protocols

ACH is governed by Nacha, ensuring secure transactions with the ability to stop or reverse payments. SWIFT uses encryption and standardized messaging for secure transactions but is harder to reverse. Lightspark enhances security with Bitcoin’s decentralized foundation and self-custodial wallets, ensuring robust protection against unauthorized access.

Operational Hours

ACH operates during standard banking hours with multiple daily batch processing windows. SWIFT does not have explicit operational hours but is affected by the banks involved. Lightspark’s infrastructure is always on, enabling 24/7 payments and ensuring money moves instantly, like information on the Internet.

How ACH And SWIFT Are Used

Domestic Payroll

ACH is ideal for domestic payroll due to its low cost and batch processing capabilities, making it efficient for high-volume payments. SWIFT is unnecessary for domestic transactions. Lightspark offers instant, low-cost payroll processing, eliminating delays and reducing costs, making it a superior choice for businesses.

International Vendor Payments

SWIFT is commonly used for international vendor payments due to its global reach and secure transactions. However, it can be costly and slow. Lightspark provides instant, low-cost cross-border payments, eliminating intermediary fees and delays, making it a more efficient solution for international transactions.

Recurring Subscription Fees

ACH is suitable for recurring domestic subscription fees due to its low cost and pre-authorization capabilities. SWIFT is not needed for domestic subscriptions. Lightspark enables seamless, real-time payments for both domestic and international subscriptions, ensuring timely and cost-effective transactions.

Freelancer Payments

SWIFT is often used for paying international freelancers but can be expensive and slow. ACH is limited to domestic payments. Lightspark offers instant, low-cost payments globally, ensuring freelancers receive their funds quickly and without high fees, enhancing satisfaction and reliability.

Time for a New Standard

Lightspark is a global payments infrastructure provider that enables real-time, cross-border money movement using Bitcoin, fiat, and stablecoins. Compared to ACH and SWIFT, Lightspark offers faster settlement, lower fees, and greater accessibility for international transactions.

- Built on Bitcoin: Lightspark’s infrastructure leverages Bitcoin’s decentralized foundation, integrating with the Lightning Network for fast, low-cost transactions.

- Instant Settlement: The platform enables instant settlement of payments across borders and currencies, reducing float and unlocking 24/7 payments.

- Lower fees: By utilizing Bitcoin and the Lightning Network, Lightspark reduces transaction fees and eliminates hidden costs, making payments more affordable.

- Cross-border security by default: Lightspark ensures secure, reliable cross-border payments by leveraging Bitcoin’s decentralized and secure foundation, with built-in compliance features for regulated institutions.

A Modern Infrastructure

For businesses looking to move beyond traditional payment systems like ACH and SWIFT, here’s what Lightspark has to offer:

- Wallets: Build feature-rich digital wallets with flexible custody options, supporting Bitcoin, Lightning, and stablecoins.

- Digital Banks: Connect to the 'Money Grid' to expand reach, improve efficiency, and offer advanced payment capabilities.

- Exchanges: Easily connect to the Bitcoin Network for instant, powerful Bitcoin movement and lower transaction costs.

- Stablecoins: Use Spark to create, distribute, and monetize stablecoins on the Bitcoin network quickly and cost-effectively.

Emerging technologies and evolving regulations are reshaping the future of payments. Lightspark can help businesses achieve real-time, low-cost global payments. Don’t just choose between two outdated options—upgrade to a payment rail built for the internet age. Learn more or book a demo.