Move beyond payouts. Give creators a branded account that holds, moves, and spends the money they earn with you.

Grid Global Accounts

(0, 0, 0)

The platform creates the income. But someone else gets the account.

Creator platforms have built some of the best earning experiences on the internet. Subscriptions, tips, transactions, and commissions all happen because your product put the audience, the catalog, and the trust in the same place. The income exists because the platform exists.

Then the payout runs, and the financial relationship moves elsewhere. A processor sends the money. A bank holds it. A card issuer monetizes the spend. An FX provider takes the spread. By the time a creator checks their balance, they're checking it inside someone else's product.

The global account

Stop sending the relationship away. Give creators the account in your product.

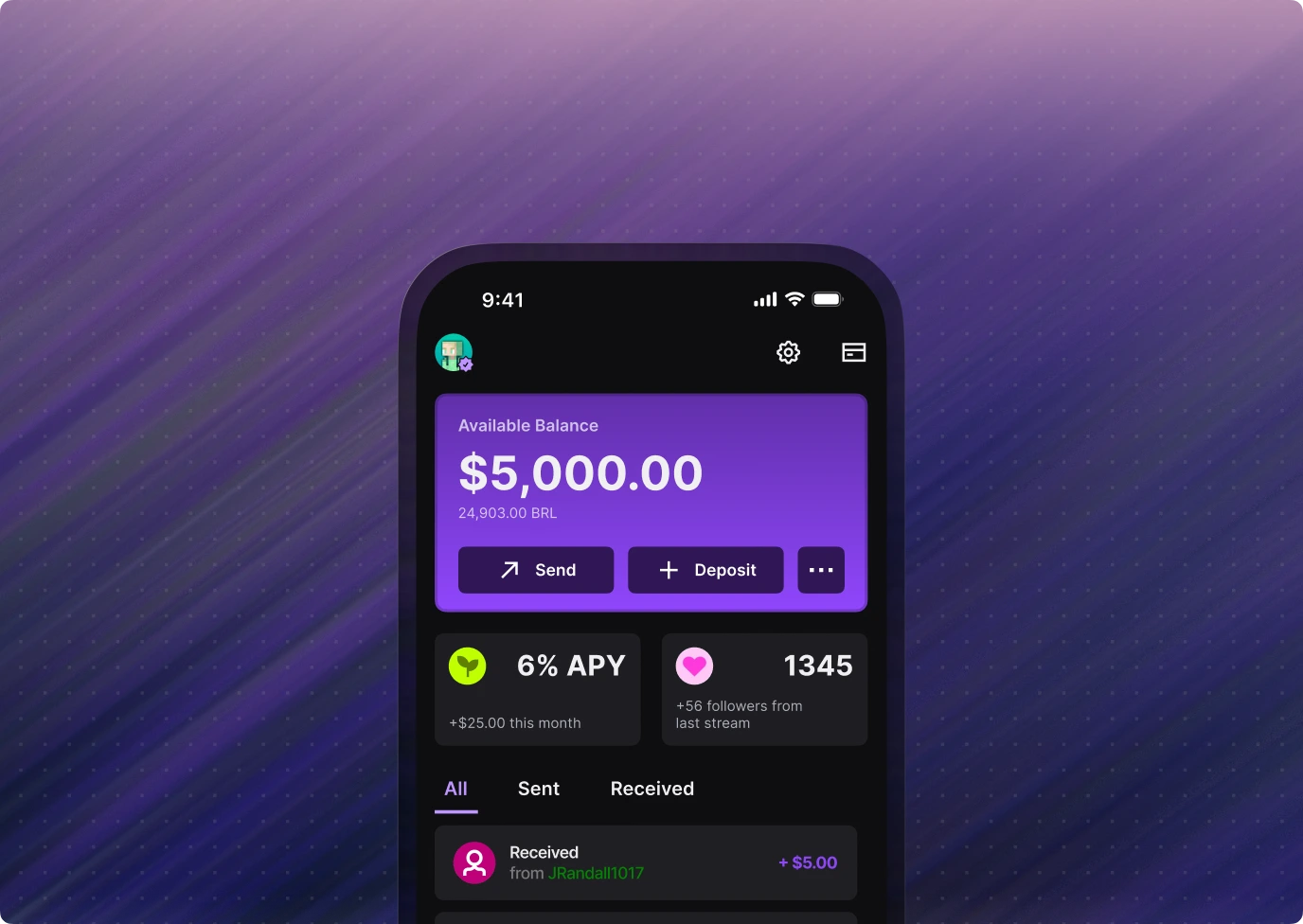

Grid Global Accounts changes how the payout ends. Creator earnings land in a branded dollar account inside your product. Creators use that balance from where they already are, with no separate banking app to open.

The account isn't a financial bolt-on. It's where the money lives, and where the decisions about it happen.

Creator earnings land in a dollar balance under your brand, with Lightspark powering the account infrastructure underneath.

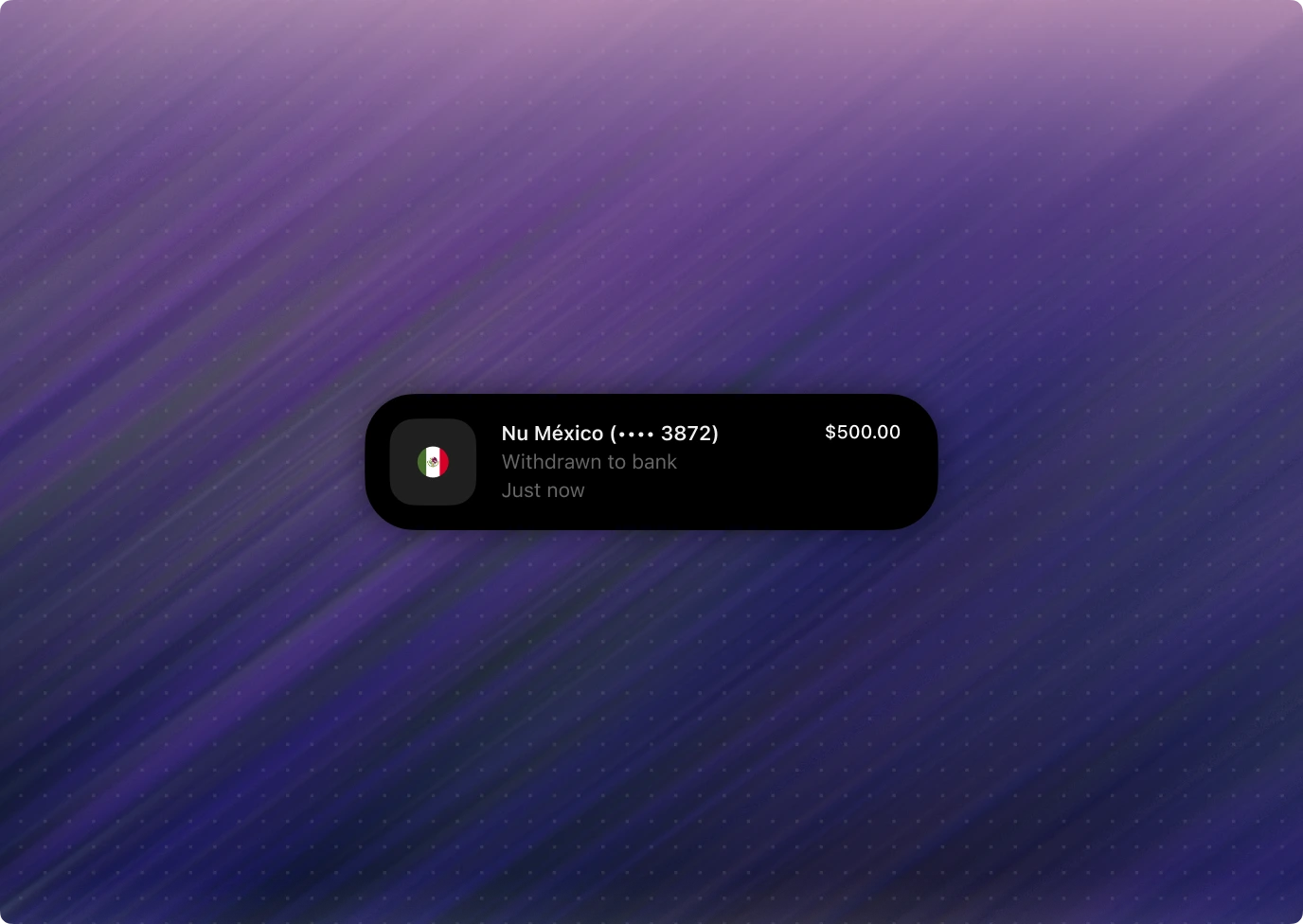

Real-time off-ramps to local and global banking rails, including PIX, UPI, SEPA, FPS, and more corridors coming online.

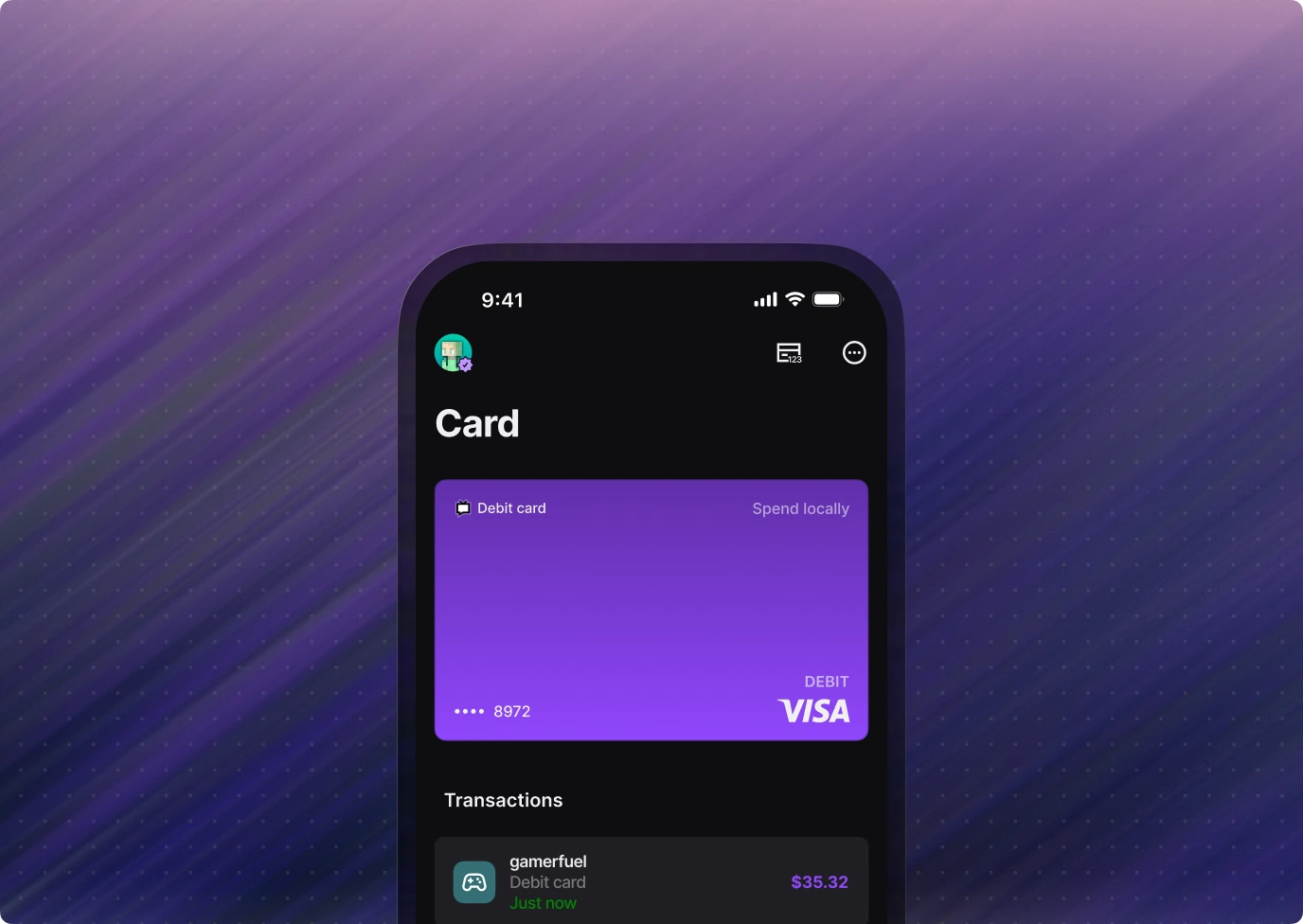

Creators can spend their balance with virtual or physical cards, locally and globally, anywhere Visa is accepted.

Move dollars into USDC, USDT, USDB, and other supported stablecoins across Base, Solana, Ethereum, Spark, Arbitrum, Tron, and more.

Because Global Accounts run on Spark, creators can hold Bitcoin alongside dollars and swap instantly without leaving the account.

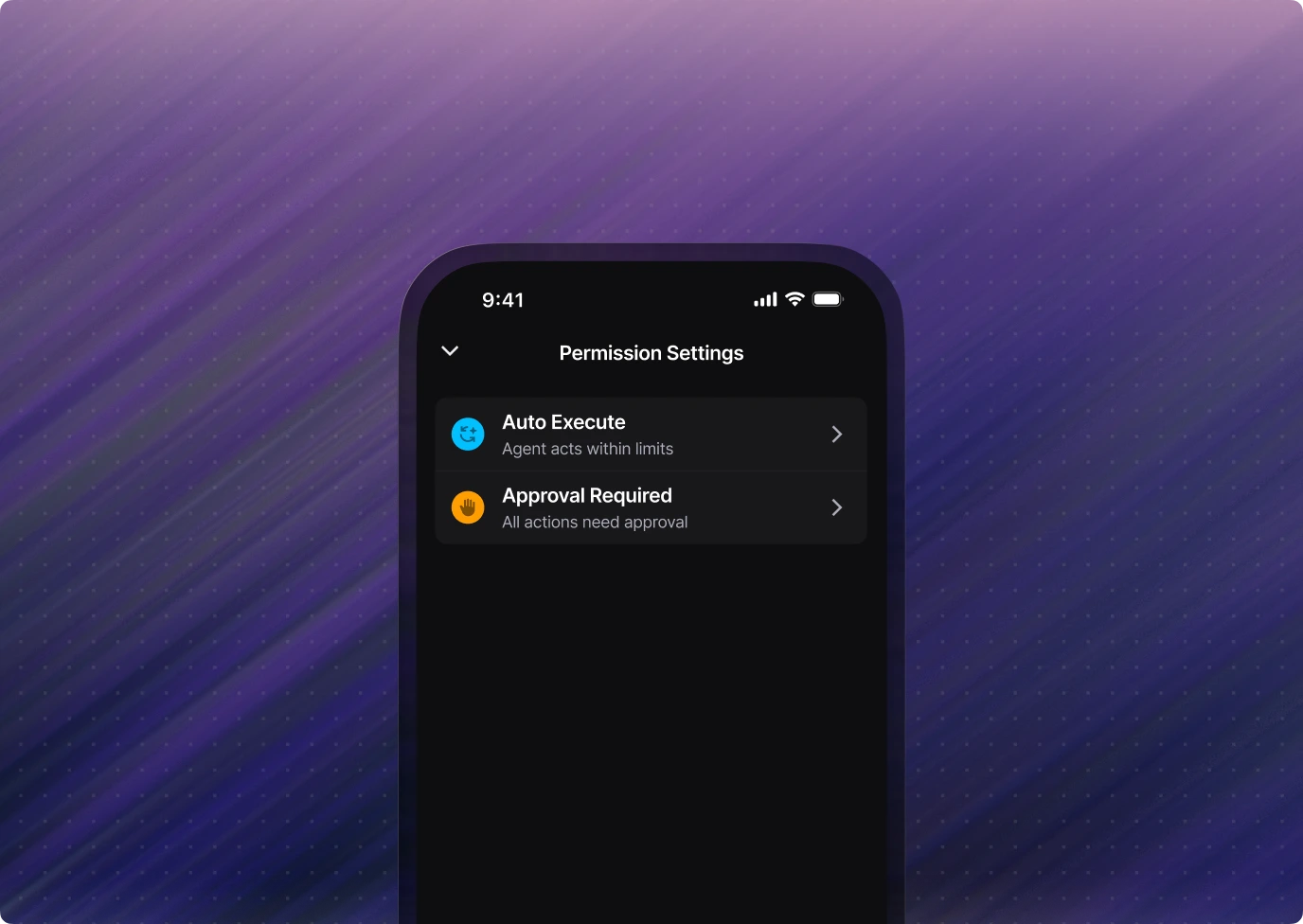

Give agents narrow budgets, approved rails, and approval thresholds so they can help operate the account without holding the keys.

The economics

Creators can hold, spend, and cash out. You own the economics.

Most platforms still treat payouts as cost. Every transfer is a fee. Every cash-out is a handoff. Every balance that leaves is wallet share another company gets to monetize.

Accounts invert that. Balances earn yield. Cards generate interchange. Foreign exchange carries margin. Bitcoin trading carries spread. When the account belongs to the platform, those flows accrue back to it. Every reason a creator keeps their money in the account is another reason to keep making the account better. The product gets stickier as the relationship gets deeper.

Creators come to earn. They stay to manage the money.

Security & compliance

Ship the account. Not the bank behind it.

Shipping an account used to mean shipping the regulated machinery underneath: money transmission, KYC, sanctions screening, custody, dispute handling, security review, and partner operations. Most platforms looked at that list and decided their core product was a better place to spend their energy. Grid Global Accounts carries that side of the equation so your team doesn't have to.

The accounts themselves are self-custodial and built on Spark. Neither Lightspark nor the platform can unilaterally move user funds. That makes the policy and approval model real, with boundaries enforced by architecture instead of trust.

Outbound movement requires the creator to authorize from their wallet. The platform can design the flow, limits, and approvals, but the account owner stays in the loop when funds leave.

Global Accounts are built on Spark wallets, so account control is enforced at the wallet layer. Neither Lightspark nor the platform can unilaterally move user funds.

Lightspark Payments is registered with FinCEN as a money services business and holds money transmission licenses or registrations where required for Grid Transaction Services, with banking and payment partners behind the regulated rails.

Lightspark handles the operational work platforms do not want to rebuild: identity checks, business verification, sanctions screening, risk review, and the compliance requirements attached to supported corridors.

The infrastructure is backed by Lightspark's security program, audited under SOC 2 Type II with NIST CSF–aligned controls, so teams can evaluate the account layer like enterprise financial infrastructure.

You own the brand, UX, account rules, approval flows, and user experience. Lightspark powers the account and regulated movement underneath.

Standard Grid objects and webhooks keep funding, withdrawals, card activity, quotes, and settlement status visible to your team instead of hiding money movement in a black box.

Integration

One Grid integration. Live in weeks, not years.

This is not a multi-year banking build. Your team starts with one API, a sandbox, and the normal objects you would expect: customers, accounts, quotes, transactions, and webhooks. Create the customer, fetch the Global Account, fund it in sandbox, and test the full request shape before production money moves.

The hard parts are already packaged: account provisioning, supported rails, wallet authorization, simulated funding, webhook events, and signed withdrawals. The Grid docs give your team the implementation path: OpenAPI, copyable examples, sandbox test credentials, Postman collections, and AI-readable pages.

Agentic money

Creator work is becoming agentic. The account needs to keep up.

Creators are already using agents to publish, plan, buy, book, and reconcile. The next obvious step is moving money on a creator's behalf. The interesting question isn't whether agents will spend from creator accounts. They will. The question is what enforces the boundaries when they do.

Letting an agent touch money without a policy boundary, an approval flow, or an audit trail is how good intentions become bad outcomes. The account is what makes that safe.

The agent gets a pocket, not the keys. Policy decides what is allowed, the account enforces it, and the creator stays in control.

Closing

Creator tools helped creators earn. Now they help them operate.

Creators already use your platform to make money. The next step is helping them run the money: paying collaborators, reconciling expenses, moving funds between projects, delegating spend, and keeping control as their business gets more complex.

That only works if the account lives inside the platform. Not as a payout destination. As the operating layer.

Creators already earn with you. Give them an account worth staying for.

Your brand. Your economics. One integration.