Give users a branded account where conversations already happen: hold, send, spend, and cash out without leaving your platform.

Grid Global Accounts

(0, 0, 0)

Money starts in the conversation. The account lives somewhere else.

People already coordinate money in messaging products. They split costs in group chats, pay sellers, send family support, tip community members, settle local services, buy from small businesses, and make decisions with the people they trust.

But when money actually moves, the relationship leaves. A wallet opens. A bank app takes over. A payment processor owns the flow. The platform keeps the conversation, but loses the account, the balance, the transaction economics, and the context around what the payment was for.

Messaging platforms see the social graph and the transaction intent before anyone else. The missing layer is the account those decisions move through.

The global account

Keep money close to the conversation. Give users an account inside your platform.

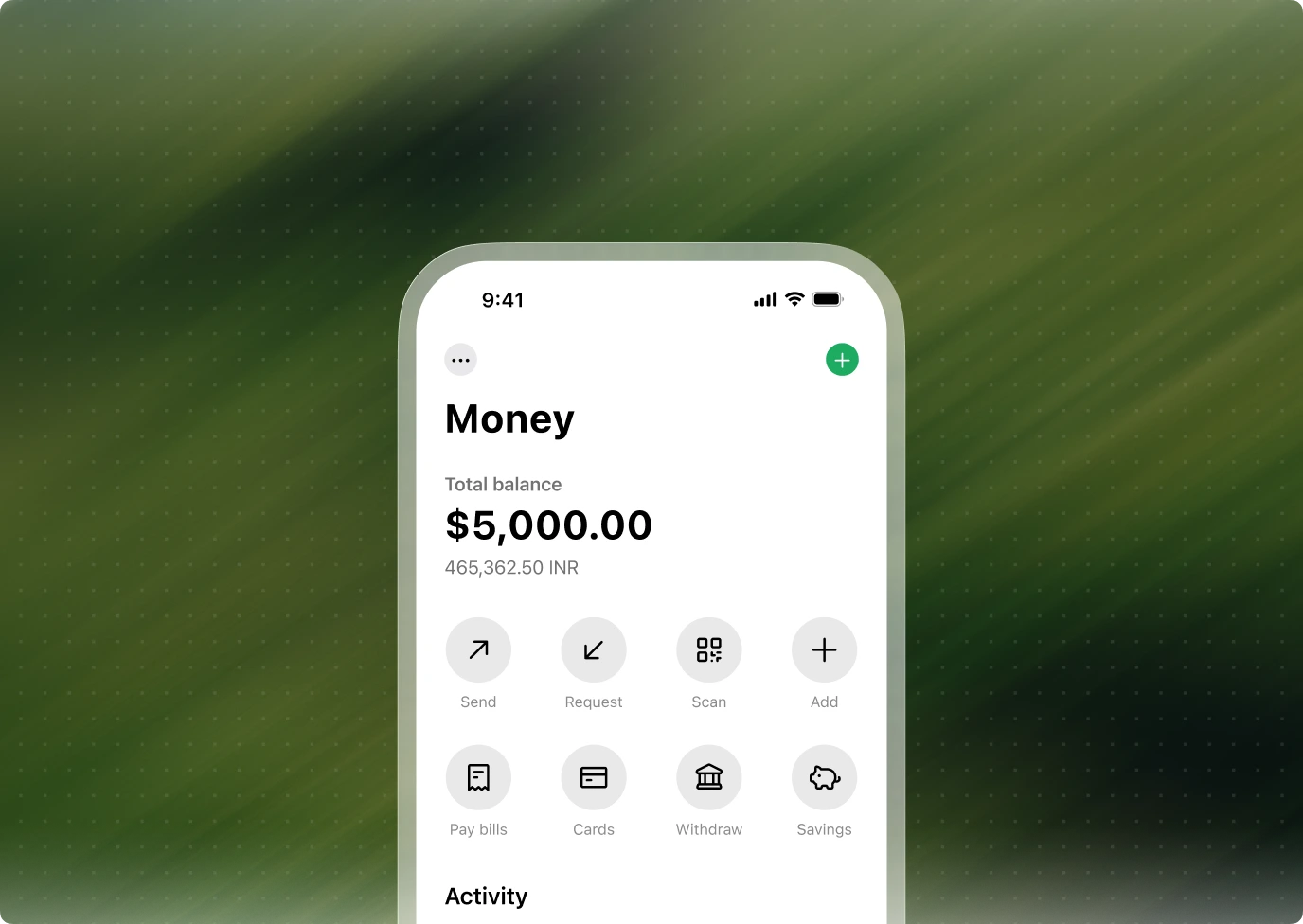

Grid Global Accounts gives every user a branded dollar account inside your messaging product. A balance can sit next to the thread, the group, the merchant chat, or the community where the money decision started.

Users can send, receive, hold, spend, cash out locally, move across stablecoin rails, hold Bitcoin, and delegate limited payment tasks without leaving your product. The account becomes the durable layer beneath conversational commerce, P2P transfers, group payments, and global support.

This is not a payment button bolted onto chat. It is the account layer for money that starts in conversation.

Give users a branded dollar balance tied to the identity, trust, and context already established in your messaging product.

Support payment actions from the surface where intent starts: group chats, merchant conversations, communities, and user profiles.

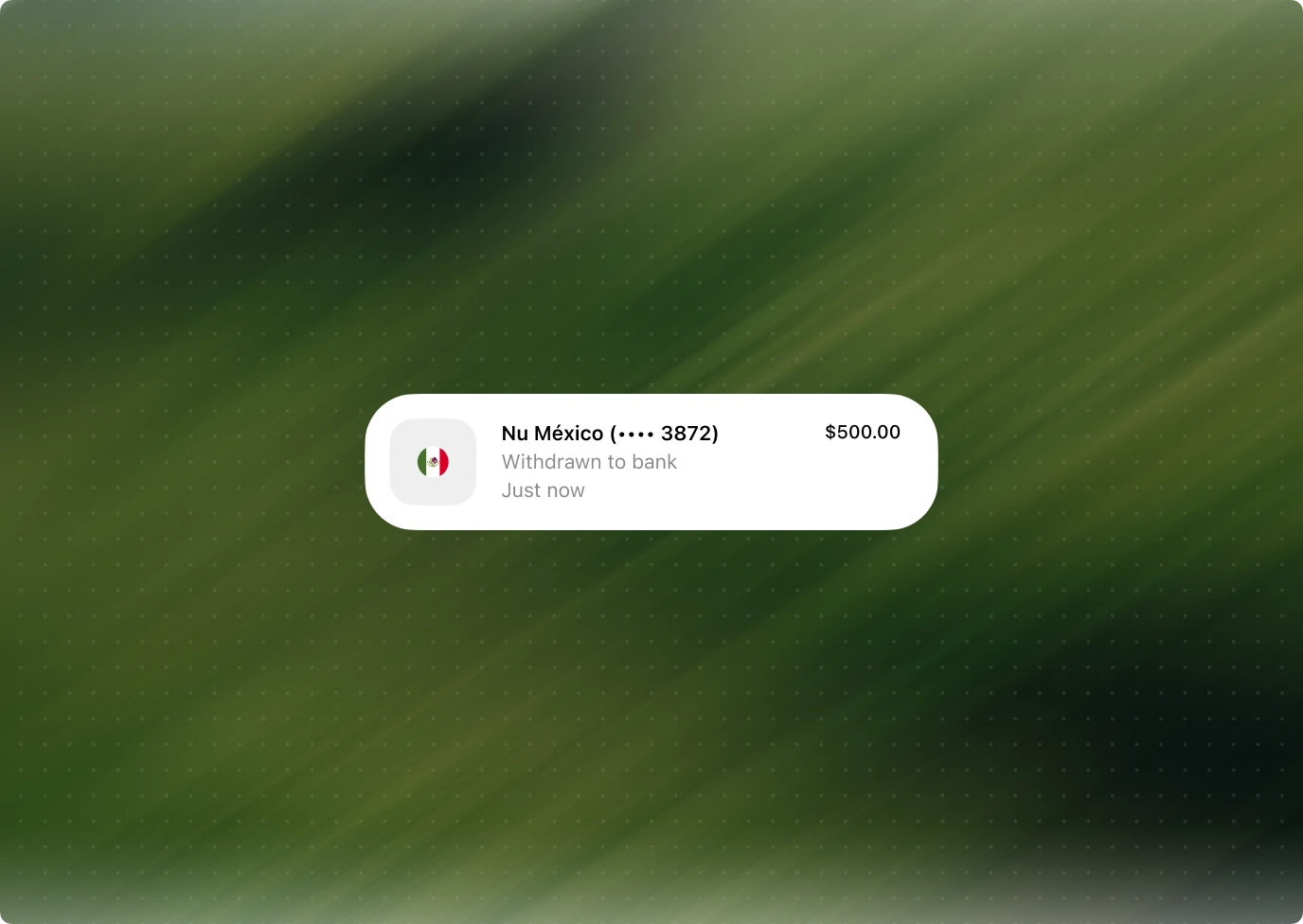

Let users move balances to local and global banking rails, including PIX, UPI, SEPA, FPS, and more supported corridors.

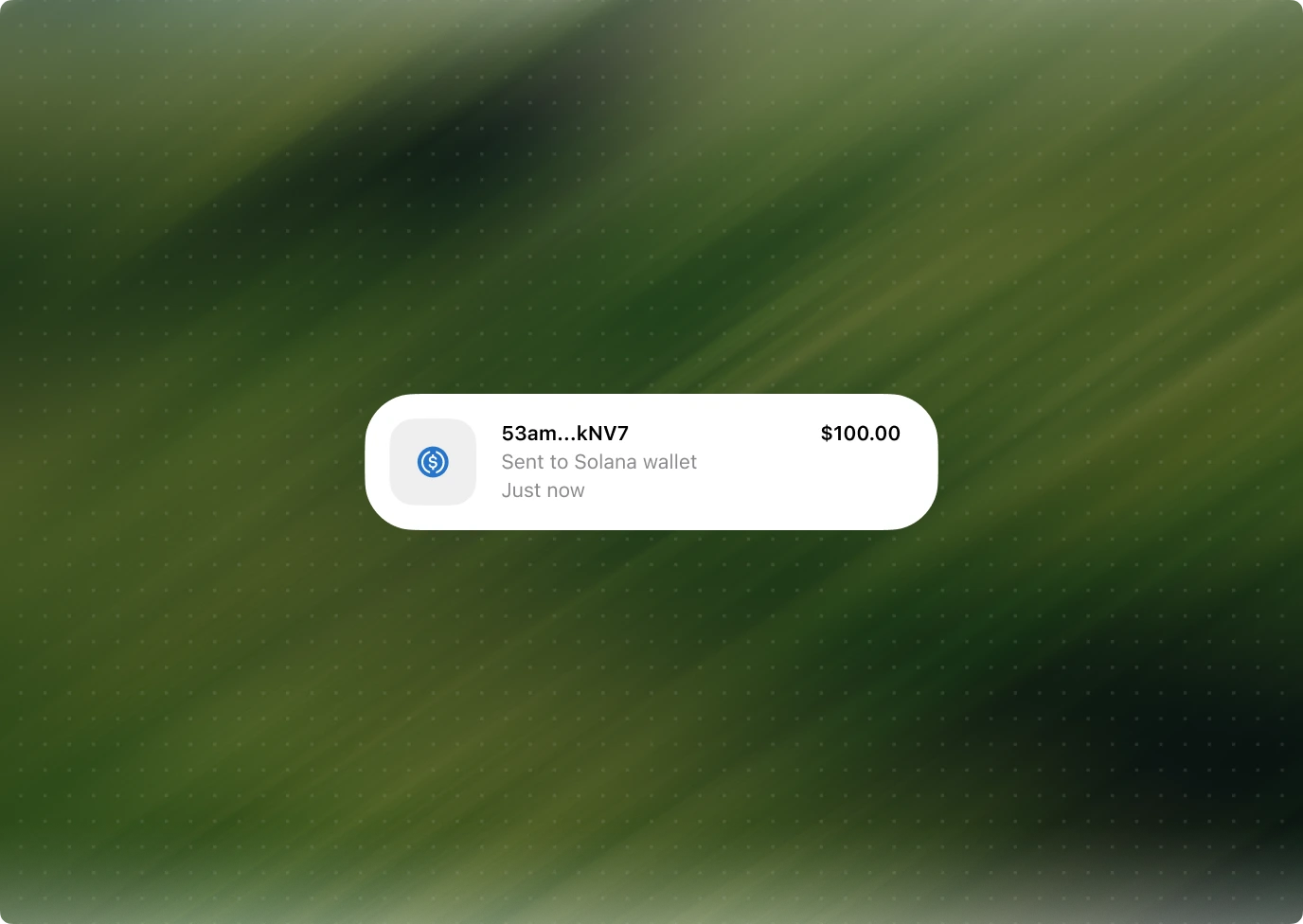

Move dollars into USDC, USDT, USDB, and other supported stablecoins across Base, Solana, Ethereum, Spark, Arbitrum, Tron, and more.

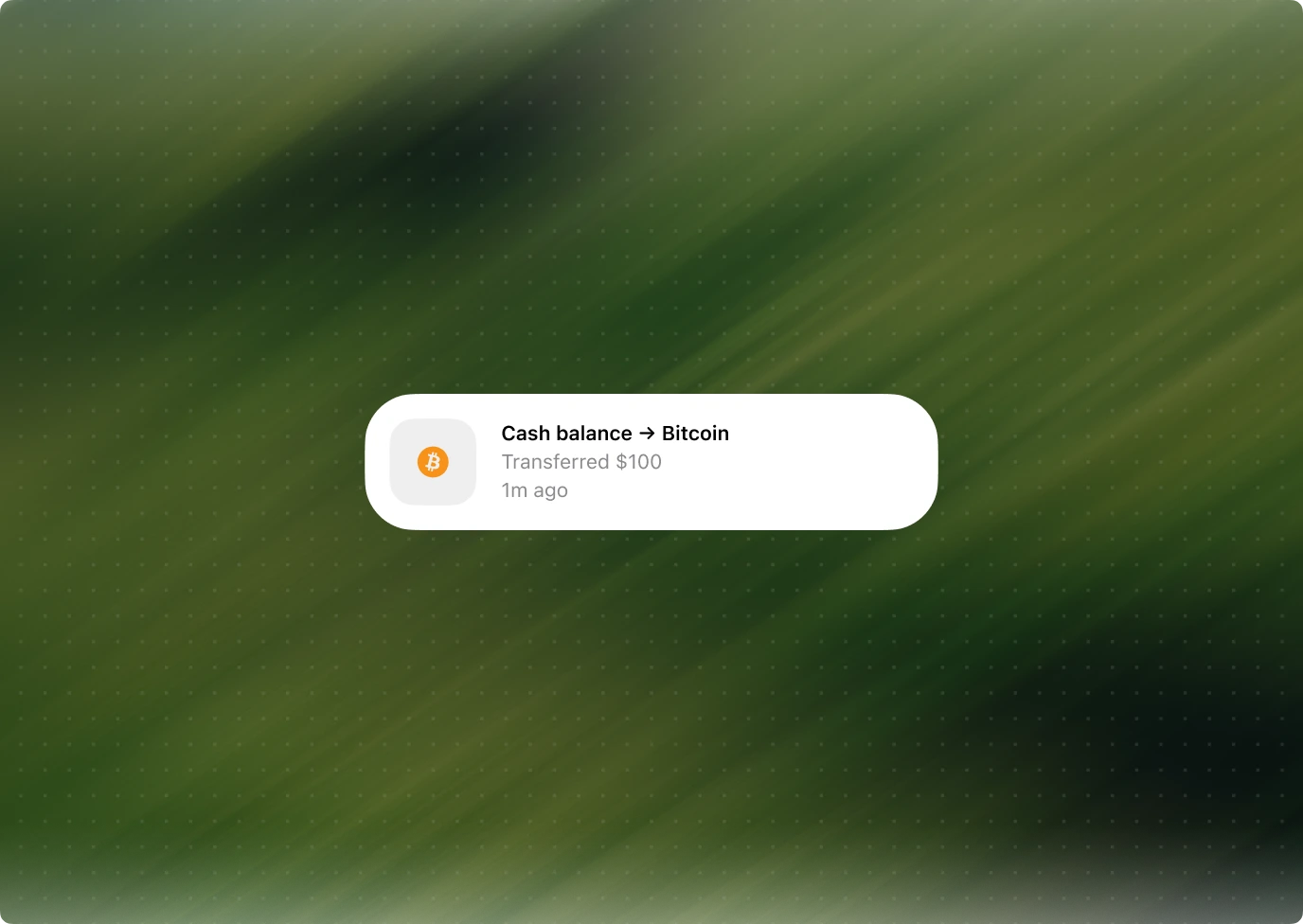

Because Global Accounts run on Spark, users can hold Bitcoin alongside dollars and swap instantly without leaving the account.

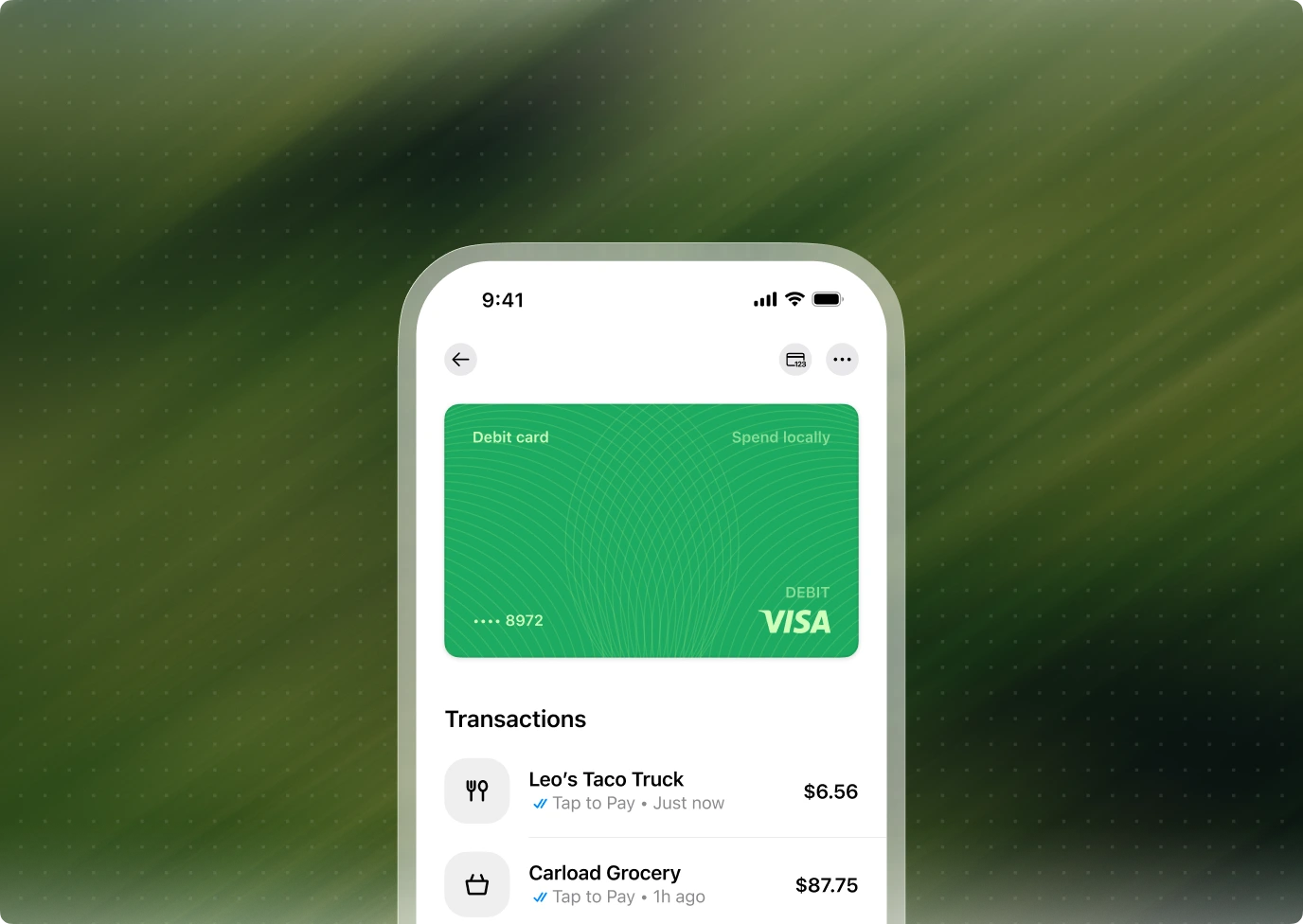

Give users a way to spend account balances beyond the conversation, locally and globally, anywhere Visa is accepted.

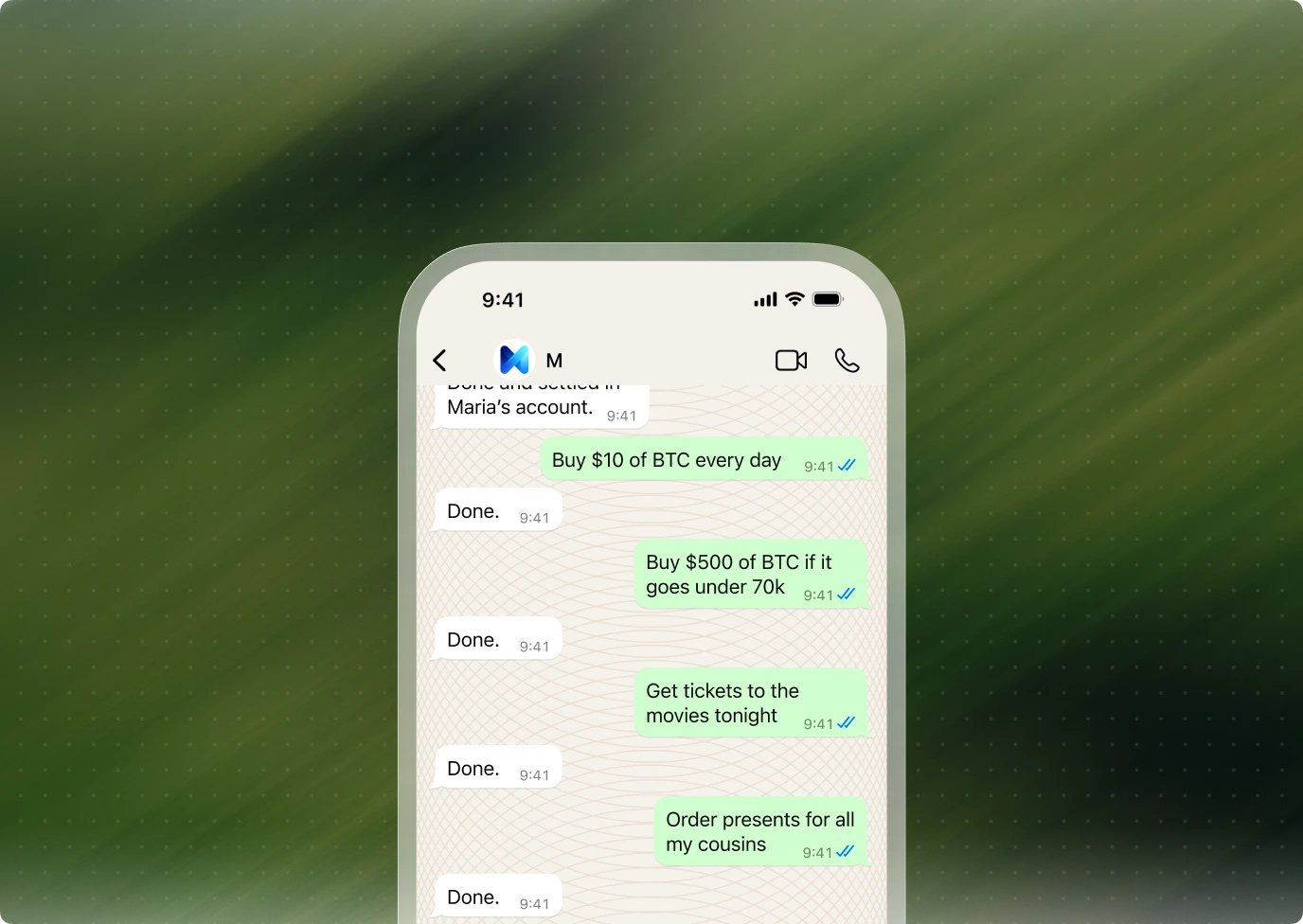

Enable policy-bound delegation for group payments, merchant chat, and business coordination without giving agents the keys.

The economics

Every payment can deepen the account. You own the economics.

Messaging platforms usually monetize attention, subscriptions, ads, or commerce adjacency. The money itself often passes through someone else's account layer. That means the most valuable financial moments in the product become payment links, external wallets, or processor flows.

Accounts change the model. Balances can stay inside the platform. P2P and merchant payments can move through your product. Cards generate interchange. FX carries margin. Reserve balances generate yield. Bitcoin trading carries spread. The more useful the account becomes, the more reasons users have to keep money where the conversation already happens.

The platform does not just host the decision. It participates in the financial relationship that follows.

Security & compliance

Add money to messaging. Not a bank build behind every chat.

Money inside conversations needs stronger boundaries than a simple payment link. Users need control over what leaves their account. Platforms need controls for risk, fraud, approvals, identity, disputes, and auditability. Agents and group workflows need limits before they ever touch funds.

Grid Global Accounts packages the regulated and operational work underneath the account layer: wallet authorization, compliance operations, supported rails, sanctions screening, identity workflows, security controls, and the infrastructure needed to move money across corridors.

The accounts are self-custodial and built on Spark. Neither Lightspark nor the platform can unilaterally move user funds. That makes account control real, with authorization enforced at the wallet layer.

Outbound money movement requires the account owner to authorize from their wallet. Messaging flows can prepare the action, but the user stays in control when funds leave.

Global Accounts are built on Spark wallets, so account control is enforced at the wallet layer. Neither Lightspark nor the platform can unilaterally move user funds.

Platforms can design limits, approvals, and account flows around groups, merchant chats, user roles, and payment thresholds.

Lightspark handles identity checks, business verification, sanctions screening, risk review, and the compliance requirements attached to supported corridors.

Lightspark Payments is registered with FinCEN as a money services business and holds money transmission licenses or registrations where required for Grid Transaction Services, with banking and payment partners behind the regulated rails.

Standard Grid objects and webhooks keep funding, payments, withdrawals, quotes, card activity, and settlement status visible instead of hiding money movement in external flows.

The infrastructure is backed by Lightspark's security program, audited under SOC 2 Type II with NIST CSF–aligned controls, so teams can evaluate money inside messaging like enterprise financial infrastructure.

Integration

One Grid integration. Money actions where users already talk.

Your team starts with one API, a sandbox, and the objects needed to build the account experience: customers, accounts, quotes, transactions, and webhooks. Create the user, fetch the Global Account, fund it in sandbox, and test the full request shape before production money moves.

The hard parts are already packaged: account provisioning, wallet authorization, supported rails, simulated funding, webhook events, signed withdrawals, and the infrastructure behind compliant money movement. Your product team decides where the account appears: a balance in the profile, a send button in the thread, a cash-out flow in settings, a merchant payment inside chat, or an approval prompt for a group.

Agentic money

Conversations are becoming agentic. The account needs policy.

Agents will increasingly sit inside conversations: scheduling, buying, collecting, reconciling, reminding, routing, and preparing payments. In messaging products, that can be useful fast. It can also become risky fast if the agent has broad access to money.

Grid Global Accounts gives agents scoped authority instead of account ownership. The agent can prepare a payment, collect from a group, pay an approved merchant, or route a business expense. Policy defines what is allowed. The account enforces it. The user approves what crosses the line.

The agent gets a mandate, not the keys.

Closing

Messaging platforms host the decision. Now they can host the account.

Money does not start in a checkout flow. It starts when people agree, ask, sell, support, split, tip, buy, and coordinate. For messaging platforms, that moment already happens inside the product.

Grid Global Accounts turns that intent into an account relationship. Users can hold money where the conversation happens, move it across rails, spend it with cards, cash out locally, and delegate bounded tasks as workflows become more complex.

The future of money in messaging is not another external payment link. It is a branded account inside the conversation.

Your brand. Your economics. One integration.