.png)

Cross-border payments are the foundation of the global economy. They power international trade, enable remittances, support global payroll, and allow digital marketplaces to operate across borders. Yet despite their importance, moving money between countries has long been slow, expensive, and opaque. Traditional systems were built for a different era, one defined by manual processes, correspondent banking relationships, and fragmented settlement infrastructure.

Today, expectations have changed. Businesses and consumers alike now demand instant transfers, predictable costs, and real-time visibility. This shift is driving a new wave of innovation in global payments, including modern settlement networks like Lightspark Grid, which are redefining how value moves across borders by making it faster, more transparent, and programmable at scale.

What Are Cross-Border Payments?

At their simplest, cross-border payments are financial transactions in which the sender and recipient are located in different countries. While the concept of cross-border transactions appears straightforward, the execution is anything but. Each transaction must navigate currency conversion, regulatory requirements, compliance checks, and multiple financial institutions before settlement is complete.

These payments support a wide range of real-world use cases, from international e-commerce and B2B supplier payments to freelance payouts, global payroll, and remittances. Behind every transaction is a complex web of banks, payment service providers, and messaging standards that must coordinate flawlessly. This underlying complexity is the root cause of many long-standing inefficiencies in the system.

The Traditional Cross-Border Payment Landscape

For decades, cross-border payments have relied on correspondent banking networks supported by the SWIFT messaging system. SWIFT enables banks to securely exchange standardized payment instructions, but it does not move money itself. Instead, settlement occurs through correspondent banks that hold accounts with one another—often across multiple countries—using nostro and vostro accounts to facilitate international transfers and international payments.

When two banks do not have a direct relationship, payments must pass through one or more intermediary banks. Each intermediary processes the transaction, conducts AML and sanctions checks, applies fees, and frequently performs currency conversion. While this model provides global reach and regulatory familiarity, it introduces multiple layers of friction.

In practice, traditional cross-border payment flows are constrained by several structural limitations:

- Multiple intermediaries and handoffs, which increase processing time and introduce cumulative fees

- Settlement delays, driven by banking hours, cutoff times, liquidity constraints, and manual reconciliation

- Foreign exchange inefficiencies, including FX spreads and multiple currency conversions and payment methods

- Limited transparency, making it difficult to track payment status, fee deductions, and delivery timing

- Operational and compliance complexity, as AML, KYC, and sanctions checks are repeated across institutions

Even with incremental improvements such as SWIFT GPI, which adds payment tracking and faster messaging, these underlying issues remain largely unresolved. Settlement is still not real time, costs remain high in many corridors, and transparency varies by institution.

Fintech companies have improved the front-end user experience with mobile interfaces, clearer pricing, and faster local payouts. However, many continue to rely on the same legacy payment rails behind the scenes. As a result, core challenges—including settlement delays, high fees, FX inefficiencies, and fragmented infrastructure—persist, highlighting the growing gap between traditional cross-border payment systems and the expectations of today’s always-on global economy.

Why Traditional Cross-Border Payments Struggle

The challenges facing cross-border payments are well-documented and stem from several persistent issues embedded in legacy systems:

- Foreign exchange complexity is one of the most significant pain points. Currency conversions often involve hidden spreads, fluctuating exchange rates, and multiple FX hops, which can reduce the final amount received and introduce uncertainty during multi-day settlement windows.

- Lack of transparency remains a critical concern. Senders and recipients frequently lack real-time insight into where a payment is, which fees have been deducted, or when funds will arrive. This opacity complicates reconciliation and erodes trust—especially for businesses managing high transaction volumes.

- Settlement delays are equally problematic. Depending on corridors, cutoff times, banking holidays, and regulatory reviews, cross-border payments can take days or even weeks to settle. These delays disrupt cash flow, slow supply chains, and create unnecessary friction for individuals and businesses alike.

- High and unpredictable costs continue to be a major barrier. Each intermediary in the correspondent banking chain adds fees, making international transfers disproportionately expensive for smaller payments and emerging-market recipients.

- Operational and compliance complexity further compounds these challenges. Legacy payment flows require repetitive AML, KYC, and sanctions checks across multiple institutions, increasing operational overhead, slowing processing times, and raising the risk of errors or payment failures.

Together, these issues underscore why the legacy cross-border payment system is increasingly unsustainable in a global, always-on economy. As businesses expand internationally and digital commerce accelerates, the limitations of correspondent banking become more pronounced. What once functioned adequately for low-volume, high-value transfers now struggles to support real-time payouts, global marketplaces, and modern financial applications. This growing mismatch between infrastructure and expectations is driving demand for faster, more transparent, and more programmable cross-border payment networks.

Global Efforts to Modernize Cross-Border Payments

Recognizing these challenges, regulators and industry leaders are pushing for systemic change. The G20 roadmap for cross-border payments focuses on implementing initiatives to improve speed, reduce costs, expand access, and increase transparency. One cornerstone of this effort is the global adoption of ISO 20022, a modern messaging standard that enables richer data, better compliance, and improved automation.

At the same time, blockchain and distributed ledger technology are reshaping expectations around settlement. These technologies enable near-instant value transfer, immutable records, and reduced reliance on intermediaries. Real-time domestic payment systems—such as FedNow, UPI, Pix, and SEPA Instant—are also setting a new baseline for speed. The next challenge is connecting these systems globally in a seamless, interoperable way.

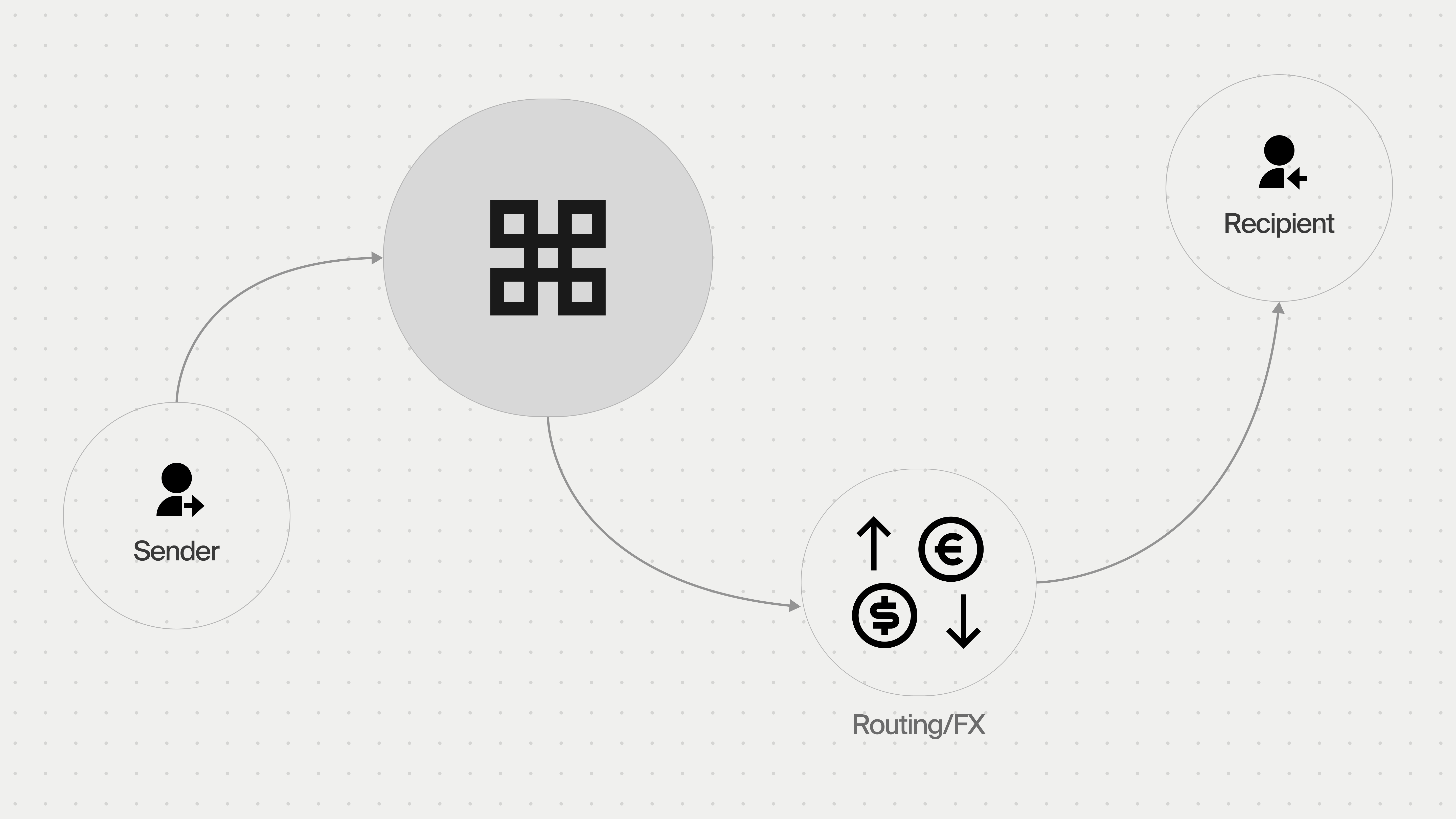

Introducing Lightspark Grid

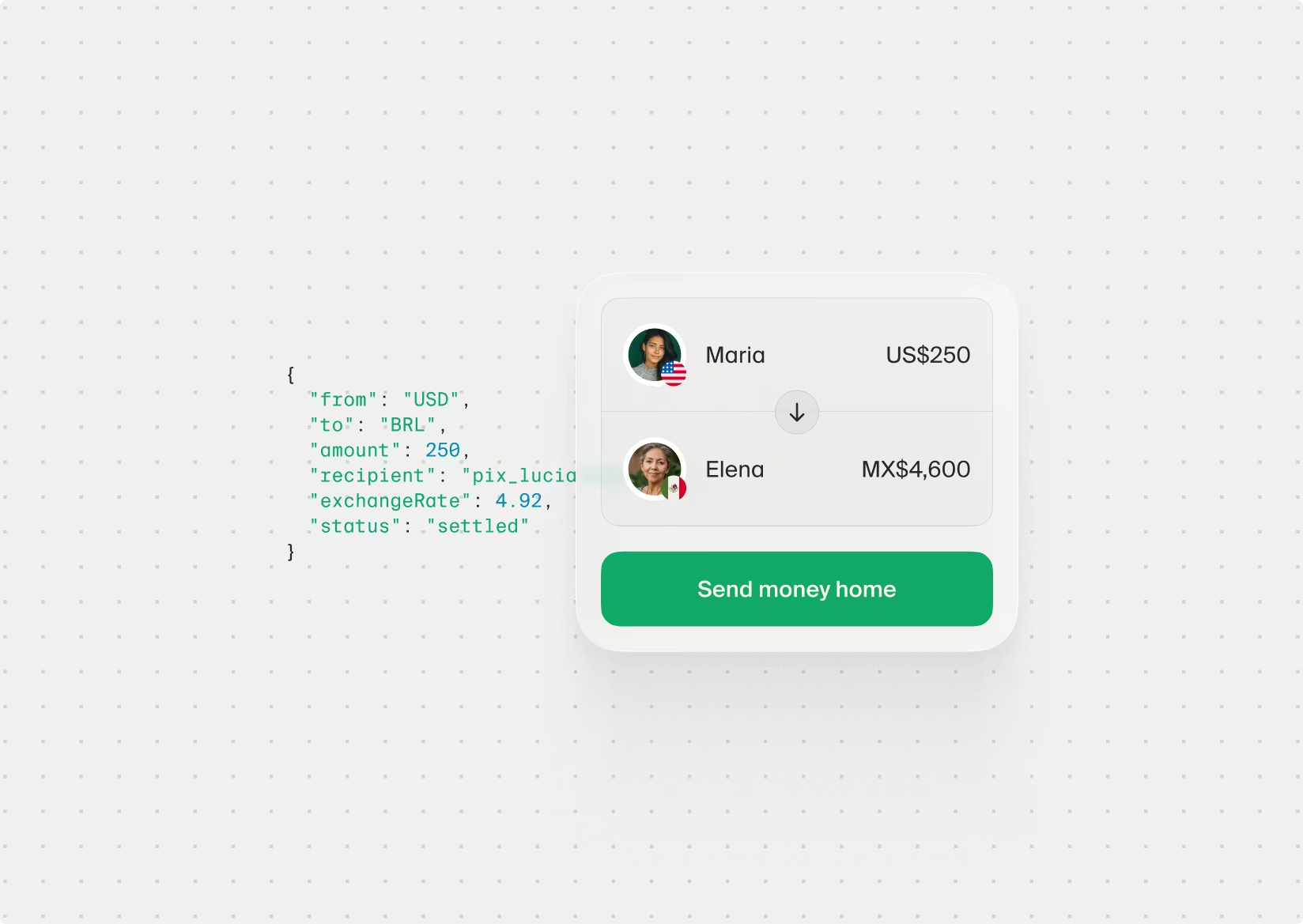

Lightspark Grid is designed to meet this challenge head-on. It is a modern global payment network and developer platform that enables instant, low-cost, and transparent cross-border payments through a single API. Rather than layering incremental improvements on top of legacy systems, Grid reimagines global settlement from the ground up.

By abstracting away the complexity of liquidity management, FX conversion, routing, blockchain operations, and compliance integration, Lightspark Grid allows businesses to move value globally without building or managing complex infrastructure. Under the hood, Grid leverages Bitcoin and the Lightning Network as a neutral, high-efficiency settlement layer—while shielding users from crypto complexity.

How Lightspark Grid Solves Core Cross-Border Challenges

Lightspark Grid addresses the most persistent pain points in cross-border payments by enabling near-real-time settlement, often within seconds rather than days. This speed dramatically improves cash flow predictability for businesses and ensures recipients gain immediate access to funds.

Costs are reduced by minimizing intermediaries and optimizing routing. With fewer parties involved and more efficient settlement rails, businesses benefit from lower transaction fees and tighter FX spreads. Currency conversion is handled automatically with real-time pricing, eliminating hidden costs and unpredictable outcomes.

Transparency is built into every transaction. Grid provides end-to-end visibility, including real-time status updates, fee breakdowns, settlement timing, and reconciliation metadata. This level of clarity improves operational efficiency and builds trust for both businesses and end users.

Importantly, Grid is designed for regulated environments. It integrates seamlessly with existing AML, KYC, KYB, and sanctions screening frameworks, ensuring compliance without sacrificing speed or scalability.

Real-World Applications Across Industries

The impact of Lightspark Grid is felt across multiple sectors, enabling faster, more efficient cross-border money movement where it matters most:

- Marketplaces can pay global sellers instantly, improving liquidity, seller satisfaction, and overall platform trust.

- Fintech companies can launch new cross-border products and payment corridors without relying on legacy banking rails or complex correspondent networks.

- Global payroll providers can eliminate settlement delays and reduce foreign exchange costs, improving financial predictability and well-being for international teams.

- B2B platforms benefit from real-time settlement, simpler reconciliation, and stronger, more reliable supplier relationships.

In each case, Lightspark Grid turns cross-border payments from an operational bottleneck into a meaningful competitive advantage.

The Future of Cross-Border Payments

Cross-border payments are entering a new era—one defined by instant settlement, transparent pricing, global interoperability, and developer-friendly infrastructure. Legacy correspondent banking models are giving way to modern networks that align with how businesses and consumers operate today.

Lightspark Grid represents this shift. By providing a unified global settlement layer, it removes friction from international money movement and enables a faster, more efficient, and more inclusive financial system. As global commerce continues to expand, the ability to move value seamlessly across borders will no longer be optional—it will be essential.

The future of cross-border payments is already unfolding, and Lightspark Grid is helping build the rails that make it possible.